Building better credit often requires a lot of patience. For many, it’s common to want your score to jump today so that you can get the apartment or car, with the lowest interest rates that you deserve. But without intention, you may not see the changes that you’re working for. It can be frustrating when you are ready to make a significant change, but as in anything, it doesn’t happen overnight. Many other individuals also face that pressure, and millions of people are looking for a clear path forward.

There are a lot of quick fixes and “hacks” to building credit, but absolute confidence comes from consistency- and choosing a plan that works with your financial situation. For many, it can be a revolving line of credit, but for a common low-risk solution, a 2-year credit builder loan may be the best option. Instead of scrambling for short-term wins that fade quickly, committing to a 24-month plan can stabilize your profile, prove your reliability, and help you save some money along the way.

The Power of a Long-Term Strategy

When you look at how credit scores are calculated, consistency is king. Lenders want to see that you can manage payments over a long period, not just for a few weeks or months. They are looking for a pattern of reliable behavior that predicts how you will handle a mortgage or a car note in the future.

According to data from myFICO, your payment history makes up 35% of your FICO® score¹. This is the most significant slice of the pie. A 2-year credit builder loan is designed to maximize this factor specifically. By making on-time payments every month for two years, you are adding 24 to 25 separate, positive marks to your credit report. This carries significantly more weight than a short-term loan that opens and closes in just a few months.

Don't Forget Credit Age

Another factor often overlooked is the "length of credit history," which accounts for 15% of your score.1 Short-term products that you close quickly can actually hurt this average age. A 24-month term keeps an account open and active for a substantial period, helping to anchor your credit age while you continue to build history.

It is also about giving yourself breathing room. Shorter terms often mean higher monthly payments to pay off the balance quickly, which can strain a tight budget. Spreading the term out over 24 months usually lowers the monthly obligation, making it easier to fit into your finances without stress.

How a 2-Year Credit Builder Loan Works with Cheers

At Cheers, we designed our plans specifically around a 24-month term because we know that time in the market beats timing the market. We aren't a bank; we're a financial technology company that partners with Sunrise Banks N.A. to help you reach your goals².

The concept is simple but powerful. Unlike a traditional loan, where you get money up front and pay it back, a credit builder loan works in reverse. You make payments first, and the money is released to you later. This structure protects you from debt while building your profile.

Here is how a Cheers 2-year credit builder loan works for you:

- You don't need good credit to start: There is no hard credit check required to apply. We believe your past shouldn't dictate your future.

- It's affordable: Cheers offers plans ranging from $24 to $144 per month³. You can pick a number that works for you right now, ensuring you never bite off more than you can chew.

- It builds savings: Your payments are held securely in a Certificate of Deposit (CD). At the end of the term, you get your savings back, minus the interest⁴.

If you are starting, knowing how to check your credit score is a vital part of the process. Watching those positive payments stack up over two years can be incredibly motivating.

The Advantage of Accelerated Reporting

One of the biggest hurdles with traditional credit building is the lag time. You open an account, but it might take a month or two before it even shows up on your report.

Cheers solves this with accelerated reporting. We report your account and first payment to all three credit bureaus within 15 days of account opening⁵. This means you don't have to wait months to see the account appear on your profile. You get the benefit of a long-term, 2-year credit builder loan, but the reporting action starts almost immediately.

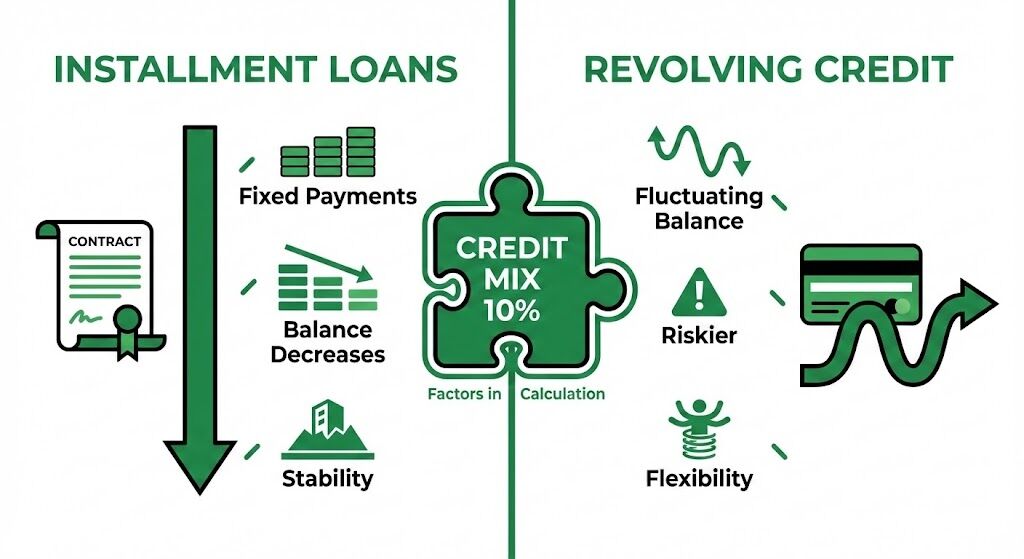

Building a Robust Credit Mix

Your credit score isn't just about paying bills on time; it's also about the types of bills you pay. Beyond payment history, 10% of your credit score is determined by your "credit mix"¹. This refers to the different types of credit you have, such as credit cards (revolving credit) and loans (installment credit).

Many people trying to build credit rely solely on secured credit cards. While these are great tools, they only represent one type of credit. If you only have credit cards, adding an installment loan like Cheers can diversify your profile. This shows lenders that you can handle different types of financial responsibilities.

Installment Loans vs. Revolving Credit

Revolving credit (like credit cards) has a fluctuating balance. Your score can dip if you use too much of your available limit. Installment loans are more stable. You pay a fixed amount every month, and the balance only goes down. This stability is often viewed favorably by scoring models. Integrating an installment loan is just one of 7 smart ways to build credit in 2025 that can help round out a healthy financial life.

Forced Savings: The Hidden Bonus

Building credit is excellent, but building wealth is better. One of the unique psychological benefits of a 2-year credit builder loan is that it acts as a "forced savings" account.

Because your payments are held in a CD until the loan matures, you are saving money every single month without thinking about it. For many people, saving money is difficult because there is always a reason to spend it. With Cheers, that money is locked away, accumulating safely.

When the two years are up, you don't just walk away with a better credit history; you walk away with a lump sum of cash (minus interest)⁴. This can be used for a down payment on a car, an emergency fund, or a deposit on an apartment. You are paying your future self, not just a lender.

Overcoming the Commitment Fear

The idea of locking yourself into a two-year contract can sound scary. Two years feels like a long time. What if you lose your job? What if you need that cash for an emergency? What if your budget changes?

These are valid concerns, and they are why flexibility is essential. A rigid financial product can become a burden if life throws you a curveball. While the Cheers plan is designed to last two years for maximum credit benefit, we don't believe in trapping you.

With Cheers, you can cancel at any time⁴. If you need to stop, you can close the account and receive the savings you have built up to that point (minus interest), with no penalty. This effectively gives you the best of both worlds: the structure and stability of a 2-year credit builder loan with the freedom of a month-to-month commitment. You can stay in the plan as long as it benefits you, without the fear of being locked into a bad situation.

Who Is This Strategy For?

A long-term credit builder loan isn't just for one type of person. It serves several different needs:

- The "Thin File" Consumer: If you have never had credit before, you have a "thin file." Lenders don't have enough data to judge you. A 2-year term creates a thick folder of data that proves you are a safe bet.

- The Rebuilder: If you have made mistakes in the past-missed payments, defaults, or bankruptcy-you need to rebuild trust. Positive new data helps outweigh the old negative data. A consistent 24-month streak of on-time payments is a powerful way to show you are back on track.

- The Newcomer: If you recently moved to the U.S., your credit history from your home country likely didn't travel with you. You are starting from scratch. Cheers allows you to start building that essential U.S. credit profile immediately.

Ready to Start Your Journey?

Fixing your credit shouldn’t be a source of constant anxiety. With all the tools available today, many are designed for specific cases, and all it takes is finding one that fits your needs and your lifestyle. Looking for long-term commitments with a low-risk solution, such as a 2-year credit builder loan, is an excellent option if you’re fixing your credit, have a thin-file, or are new to credit altogether. With Cheers Credit Builder, you get a 24-month term to build credit history, with savings at the end of your term. It’s a simple and transparent way to build your credit on your terms.

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

(The opinions expressed in this article are the author’s own and do not reflect the view of Sunrise Banks, N.A. Member FDIC.)²

References:

- What’s in my FICO Scores? - https://www.myfico.com/credit-education/whats-in-your-credit-score

1 FICO® Credit Factors: According to FICO®, 35% of your credit score is based on payment history, and 10% is based on credit mix. Cheers reports every payment and adds a secured installment loan to your profile. Source: myFICO: https://www.myfico.com/credit-education/whats-in-your-credit-score

2 Sunrise Banks: Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval. Must be at least 18 years old, have a valid U.S. bank account, and a Social Security Number.

3 Credit Builder Account Plans: All plan options include a 24-month term, 25 total payments and a 12.15% Annual Percentage Rate (APR). Plan A: Total Payments of $600 with $532.70 Amount Financed. $24 Monthly Payments and $67.30 Total Interest.Plan B: Total Payments of $825.02 with $733.13 Amount Financed. $33 Monthly Payments and $91.89 Total Interest.Plan C: Total Payments of $1,149.98 with $1,021.69 Amount Financed. $46 Monthly Payments and $128.29 Total Interest.Plan D: Total Payments of $3,600.00 with $3,197.82 Amount Financed. $144 Monthly Payments and $402.18 Total Interest.

4 Cancel Anytime & Get Savings Back: At the end of your term, your total savings (minus interest) is returned to you. You can cancel your account at any time without penalty.

5 Accelerated Reporting: Accelerated reporting applies to the opening of your account, plus the first payment. Credit bureau reporting occurs monthly thereafter

.png)