Building credit- whether starting fresh or trying to recover from the past- may seem overwhelming. With many options on the market now, some may look towards a 12-month credit builder loan or a 24-month credit builder loan. Both being viable options, a two-year timeline may be the most manageable- especially if your financial situation fluctuates unexpectedly. Nonetheless, it's essential to choose the right plan for your credit journey, and to keep in mind that the right plan is more than just speed. It's about how comfortably the payments fit into your life and whether the structure helps you stay consistent.

Before comparing different timelines, it helps to understand how credit builder loans work in general and how a steady plan—whether twelve months or twenty-four—can help shape a stronger credit foundation.

How Credit Builder Loans Work

A credit builder loan is meant to help people strengthen their credit history while saving money at the same time. With this type of loan, you don't receive funds up front. Instead, you make monthly payments that are held safely in a Certificate of Deposit (CD). Each month, your payment activity¹ is reported to all three major credit bureaus. Because payment history and credit mix make up significant portions of a FICO® score², this steady reporting can help build those areas of your profile.

For people beginning their credit journey, How to Start Building Credit explains simple habits that help shape your financial foundation, including monitoring your credit reports and focusing on consistent payments.

When your term ends, you receive your savings back minus interest. This creates a structured, low-pressure approach to building credit without taking on new debt. The system is designed to help you show responsible payment behavior, which is often the piece missing for people with thin or limited credit histories.

What Is Cheers Credit Builder?

Cheers Credit Builder follows this same foundation while making the process predictable and straightforward. Cheers is a financial technology company that helps customers build credit through a secured installment structure. There's no hard credit check to get started. Everyone goes through identity verification, but the process doesn't affect your credit score. Cheers charges a fixed 12.15% APR with no application fees, no maintenance fees, and no membership fees³.

Your monthly payments are held in a CD at Sunrise Banks, N.A. Member FDIC. Cheers reports your payment activity to all three major credit bureaus every month. Cheers offers four payment plans, all set on a 24-month term with 25 total payments⁵. This longer timeline helps keep monthly payments predictable and easier to manage. Cheers also uses accelerated reporting⁴, meaning your account and first payment can be reported within 15 days of opening your account, giving you a faster start on your credit-building journey.

What Is a 12 Month Credit Builder Loan?

Many credit builder loans in the market are structured around a 12-month timeline. This setup appeals to people who want to complete their credit-building efforts within a single year. A shorter plan can feel motivating because:

- You can see progress quickly.

- The finish line stays in sight.

- You're able to align the timeline with personal goals such as preparing for a lease, refinancing, or applying for a credit card.

A 12-month plan works well for people who are comfortable taking on a higher monthly payment in exchange for completing the process sooner. For those who have room in their budget and want a focused, time-bound approach, this structure fits naturally.

Why Some People Prefer a 12-Month Timeline

A one-year credit builder loan feels appealing for several reasons:

- It creates a sense of momentum over a short period.

- It's easier to map out a year of payments and stick to it.

- People with upcoming financial goals may want their credit-building process aligned with a specific date.

- A shorter commitment can keep motivation high since every payment brings you closer to the end.

For people who want more ways to strengthen their credit toolkit, 7 Smart Ways to Build Credit in 2026 outlines simple steps that work alongside a credit builder loan, such as lowering credit utilization or using rent reporting services.

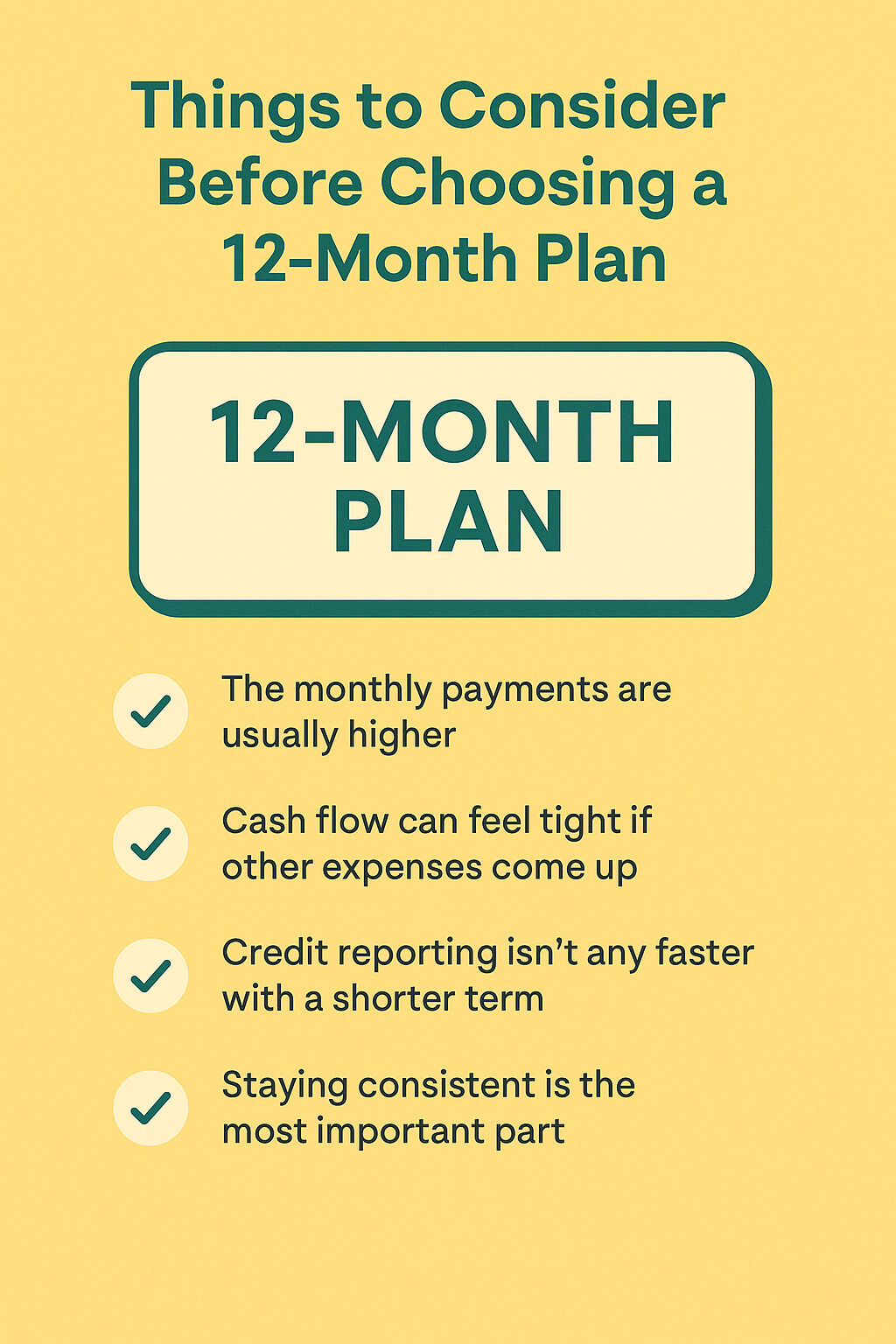

Things to Consider Before Choosing a 12-Month Plan

While a shorter term can feel energizing, it isn't always the easiest fit. Here are a few reasons some people choose a different timeline:

- The monthly payments are usually higher because the entire amount is condensed into one year.

- Cash flow can feel tight if other expenses come up.

- Credit reporting happens monthly on any timeline, so shorter terms don't speed up reporting.

- Staying consistent is the most crucial part, and higher payments may make that harder.

Government resources- like What are some ways to start or rebuild a good credit history?, reinforce that the key to rebuilding is steady, reliable payment activity—regardless of whether the plan lasts twelve months or longer. This doesn't make 12-month plans bad—they require more room in your budget.

The 24-Month Structure Explained (How Cheers Works)

Cheers uses a 24-month structure that spreads payments comfortably across two years. All four available plans follow this schedule, ranging from $24 to $144 per month⁵. This approach supports people who want a consistent structure without the pressure of higher monthly payments.

A longer runway can help because:

- The monthly cost is easier to manage.

- It's simpler to maintain steady payments.

- You still get monthly reporting to all three credit bureaus.

- You have the flexibility to cancel anytime and receive the savings you've built, minus interest⁶.

Credit building happens month by month regardless of the term length. Choosing a longer structure doesn't slow down your reporting—it simply gives you a more comfortable pace.

Choosing Between a 12-Month or 24-Month Credit Builder Loan

Both timelines support credit growth, and the right choice comes down to:

- Your monthly budget

- How quickly do you want to complete the plan

- Whether you prefer a shorter sprint or a steady, low-pressure pace

- Your financial goals for the upcoming year or two

If you're drawn to the idea of completing your payments within a year and can handle a higher monthly amount, a 12-month plan may feel right. If you want flexibility, lower costs, and a steady rhythm, a 24-month plan like the one offered by Cheers may support your needs more comfortably.

Either way, the core idea stays the same: consistent, on-time payment activity reported month after month is what helps build a stronger credit profile.

Moving Forward With Confidence

Credit building doesn't have to be a perfect process; it's about finding a plan that works within your budget. A 12-month credit builder loan offers a more limited timeline of payments, while a 24-month plan provides a more relaxed pace. Finding the pace that works within your goals and lifestyle is essential; nobody can determine that pace aside from you.

Cheers is dedicated to helping people build credit on autopilot with a straightforward, transparent approach that keeps you in control. No hard credit checks, no surprise fees, and no confusing terms—just a reliable structure designed to support your financial progress.

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

(The opinions expressed in this article are the author's own and do not reflect the view of Sunrise Banks, N.A. Member FDIC.)

References

- What are some ways to start or rebuild a good credit history? – https://www.consumerfinance.gov/ask-cfpb/what-are-some-ways-to-start-or-rebuild-a-good-credit-history-en-2155/

¹ Payment activity:

All payment activity is reported to the credit bureaus. On-time payments may help build your credit, while late or missed payments may negatively impact it. Results are not guaranteed and depend on your individual financial behavior and credit profile.

² FICO® Credit Factors:

According to FICO®, 35% of your credit score is based on payment history, and 10% is based on credit mix. Cheers reports every payment and adds a secured installment loan to your profile. Source: myFICO: https://www.myfico.com/credit-education/whats-in-your-credit-score

³ No Hidden Fees:

There are no application fees, maintenance fees, or early cancellation penalties.

⁴ Accelerated Reporting:

Accelerated reporting applies to the opening of your account, plus the first payment. Credit bureau reporting occurs monthly thereafter

⁵ Credit Builder Account Plans:

All plan options include a 24-month term, 25 total payments and a 12.15% Annual Percentage Rate (APR).

Plan A: Total Payments of $600 with $532.70 Amount Financed. $24 Monthly Payments and $67.30 Total Interest.

Plan B: Total Payments of $825.02 with $733.13 Amount Financed. $33 Monthly Payments and $91.89 Total Interest.

Plan C: Total Payments of $1,149.98 with $1,021.69 Amount Financed. $46 Monthly Payments and $128.29 Total Interest.

Plan D: Total Payments of $3,600.00 with $3,197.82 Amount Financed. $144 Monthly Payments and $402.18 Total Interest.

⁶ Cancel Anytime & Get Savings Back:

At the end of your term, your total savings (minus interest) is returned to you. You can cancel your account at any time without penalty.

.png)