Between credit cards, loans, and apps- building credit can feel like a maze when you're just starting. With every option promising quick results, it can be hard to determine which actually works. However, two popular names that come up are Cheers and Chime, which both offer a different way to build credit that varies from traditional borrowing.

While both aim to help you establish payment history and strengthen your credit profile, they take opposite paths to get there. Cheers uses a credit builder loan that enables you to save as you build, while Chime offers a secured card that lets you build through everyday spending—understanding how each one works, and which aligns with your habits, can make all the difference in your financial progress.

Let's start with how Cheers Credit Builder works and what makes its loan-based approach stand out.

What Is Cheers Credit Builder?

Cheers Credit Builder was created to make building credit predictable and straightforward. Instead of borrowing money you immediately spend, you make small monthly payments toward an account that's held securely with a partner bank. Those payments are reported to all three major credit bureaus each month¹, helping you build a consistent payment history- one of the most influential factors in your credit score².

Cheers uses accelerated reporting³, meaning your account and first payment are reported to all three major credit bureaus within days of opening. This helps you begin building credit activity earlier in your plan.

Cheers also doesn't charge setup or membership fees⁴, and there's no hard credit check to apply. You can choose a plan that fits your budget, with payments as low as $24 per month⁵. Each plan has a fixed term, and once it ends, you get back the amount you've paid, minus interest⁵.

What Is a Credit Builder Loan?

A credit builder loan is an installment-style account explicitly designed for people who want to establish or rebuild credit. Instead of giving you money up front, the lender holds your payments in a secured account. Each payment you make is reported to the credit bureaus¹, creating a track record of reliability.

Over time, that steady history can help strengthen your credit score. According to FICO®, payment history makes up 35% of your score, while credit mix, having different types of credit accounts, adds another 10%². A credit builder loan supports both of these areas, showing lenders that you can manage predictable monthly payments.

For readers just beginning their credit journey, How to Start Building Credit explores simple, step-by-step strategies to establish a strong foundation. It's a helpful resource for understanding how installment-based products like Cheers fit into the broader picture of responsible credit growth.

The structure also encourages savings, since you receive the funds at the end of the term⁵. For many people, this turns credit building into a productive habit instead of a financial risk.

What Is Chime Credit Builder?

Chime Credit Builder takes a different approach to helping you establish credit. It's a secured credit card that uses your own funds to set a spending limit, giving you control over how much you charge and pay off each month. According to the Credit Builder Credit Card - Chime, this card is designed to help members build credit safely while avoiding interest and annual fees.

To open an account, you'll need a Chime Checking Account, which connects directly to your secured card balance. The funds you move into the Credit Builder account determine your spending limit, and every on-time payment helps demonstrate responsible credit use. The How to Build Credit with Credit Builder - Chime page explains that your payment activity, account age, and current balance are reported to all three major credit bureaus, helping you create a positive payment record without traditional borrowing.

The What Is Credit Builder and How Can I Enroll? - Chime Help Center further clarifies that there's no hard credit check required to apply, and the account charges no interest or hidden fees. By pairing spending flexibility with automatic reporting, Chime's Credit Builder card offers a simple way to turn regular purchases into opportunities to grow your credit history.

What Is a Secured Credit Card?

A secured credit card is a revolving credit account backed by a refundable security deposit. The deposit acts as your credit limit, allowing you to spend against it while proving that you can repay what you borrow. Each month, the card issuer reports your payment activity and balance to the credit bureaus.

Secured cards are often a first step for people with limited or poor credit because they work just like traditional credit cards, but without requiring prior credit history. They can improve your credit score through responsible use, keeping balances low, and making on-time payments.

For a closer look at other card options that support credit building, Best Credit Cards to Build Credit in 2025: Your Guide to a Strong Financial Start breaks down several products that help new borrowers strengthen their credit safely and effectively.

However, because a secured card involves spending and repayment, it requires more discipline than a credit builder loan. If you forget to pay off your balance, it can still lead to missed payments or higher reported balances, which can hurt your score.

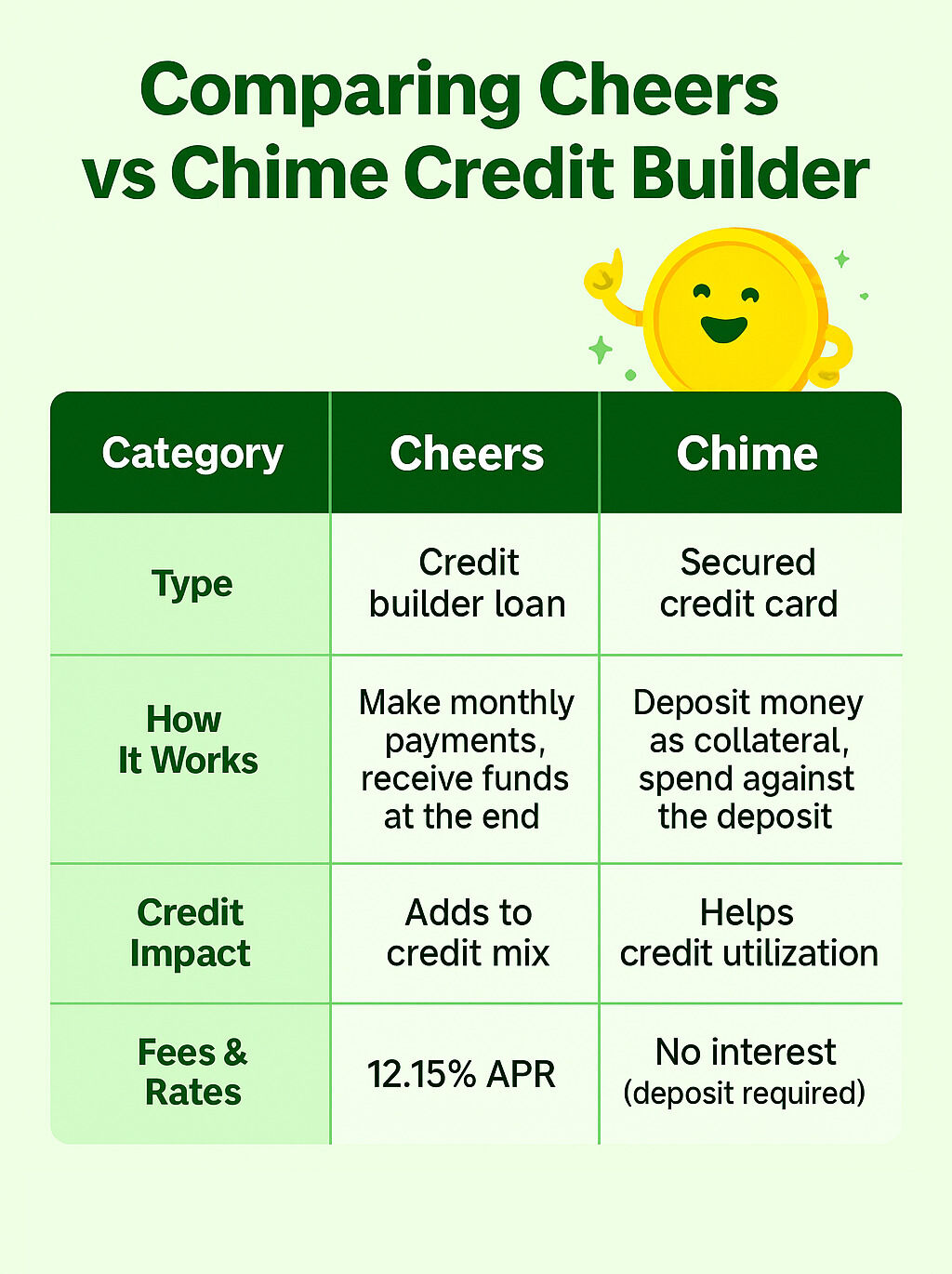

Comparing Cheers vs Chime Credit Builder

Both tools report to all three major credit bureaus and help you build positive payment history, but the way they do it-and the experience they create- differ entirely.

Cheers works through structured, automated payments that double as savings. You don't have to worry about managing balances or overspending, and you know exactly how much you'll pay each month.

Chime functions as a spending card. It's flexible, but it depends on your ability to use it wisely and pay off your balance regularly.

Key differences at a glance:

- Product type: Cheers is a credit builder loan (installment), while Chime is a secured credit card (revolving).

- Access to funds: Cheers holds your funds until your term ends⁶; Chime allows active spending up to your deposit.

- Cost model: Cheers charges a fixed, low APR; Chime charges no interest when paid in full.

- Reporting behavior: Cheers uses accelerated reporting³ where Chime reports monthly payment activity.

- Credit impact: Cheers strengthens payment history where Chime supports responsible revolving credit habits.

Which Credit Builder Fits Your Goals?

Ultimately, the decision between Chers and Chime depend on how you'd prefer to manage your money and your spending/credit habits. If you like structure, steady progress, and the idea of saving while you build credit, Cheers is the better fit. Your payments are predictable, and you finish your term with both credit history and savings to show for it.

If you prefer flexibility and already manage credit cards responsibly, Chime may suit your lifestyle. It rewards consistent use and repayment, helping you show lenders that you can handle revolving credit.

Both tools can improve your financial footing, but for those who want credit building on autopilot, Cheers keeps the process simple and secure.

Conclusion

Building credit doesn't look the same for everyone. Some people prefer the flexibility of using a card and paying it off each month, while others want a system that keeps them consistent without worrying about overspending. Both Cheers and Chime aim to make credit building more accessible, but they take very different routes to help you get there.

Chime's Credit Builder card focuses on everyday spending habits. It works best for those who are comfortable managing purchases and want the familiarity of a credit card. Cheers, on the other hand, was built for people who wish to progress without pressure. Its credit builder loan combines savings and reporting, helping you establish a solid credit history through small, predictable payments.

That approach captures the heart of Cheers' mission to make credit building simple, transparent, and stress-free. By turning monthly payments into steady progress, Cheers helps you strengthen your credit while creating a foundation of savings that grows with you. It's credit building on autopilot, designed to help you move forward confidently toward financial freedom.

Cheers is not a bank. Deposit accounts are held by Sunrise Banks, N.A., Member FDIC⁷.

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

References:

- Chime - Credit Builder Credit Card - https://www.chime.com/credit-builder/

- Chime - How to Build Credit with Credit Builder - https://chime.com/credit-builder/how-it-works/

- Chime Help Center - What Is Credit Builder and How Can I Enroll? - https://help.chime.com/hc/en-us/articles/17192694520983-What-is-Credit-Builder-and-how-can-I-enroll

Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval.

Eligibility Criteria:

Must be at least 18 years old, have a valid U.S. bank account, and a Social Security Number. All accounts are subject to identity verification and consumer report review by the issuing bank, Sunrise Banks N.A., Member FDIC.

¹ Payment Activity:

All payment activity is reported to the credit bureaus. On-time payments may help build your credit, while late or missed payments may negatively impact it. Results are not guaranteed and depend on your individual financial behavior and credit profile.

² FICO® Credit Factors:

According to FICO®, 35% of your credit score is based on payment history, and 10% is based on credit mix. Cheers reports every payment and adds a secured installment loan to your profile.

Source: myFICO

³ Accelerated Reporting:

Accelerated reporting applies to the opening of your account, plus the first payment. Credit bureau reporting occurs monthly thereafter.

⁴ No Hidden Fees:

There are no application fees, maintenance fees, or early cancellation penalties.

⁵Credit Builder Account Plans:

All plan options include a 24-month term, 25 total payments and a 12.15% Annual Percentage Rate (APR).

Plan A: Total Payments of $600 with $532.70 Amount Financed. $24 Monthly Payments and $67.30 Total Interest.

Plan B: Total Payments of $825.02 with $733.13 Amount Financed. $33 Monthly Payments and $91.89 Total Interest.

Plan C: Total Payments of $1,149.98 with $1,021.69 Amount Financed. $46 Monthly Payments and $128.29 Total Interest.

Plan D: Total Payments of $3,600.00 with $3,197.82 Amount Financed. $144 Monthly Payments and $402.18 Total Interest.

⁶ Cancel Anytime & Get Savings Back:

At the end of your term, your total savings (minus interest) is returned to you. You can cancel your account at any time without penalty.

⁷ Sunrise Banks:

Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval. Must be at least 18 years old, have a valid U.S. bank account, and a Social Security Number.

.png)