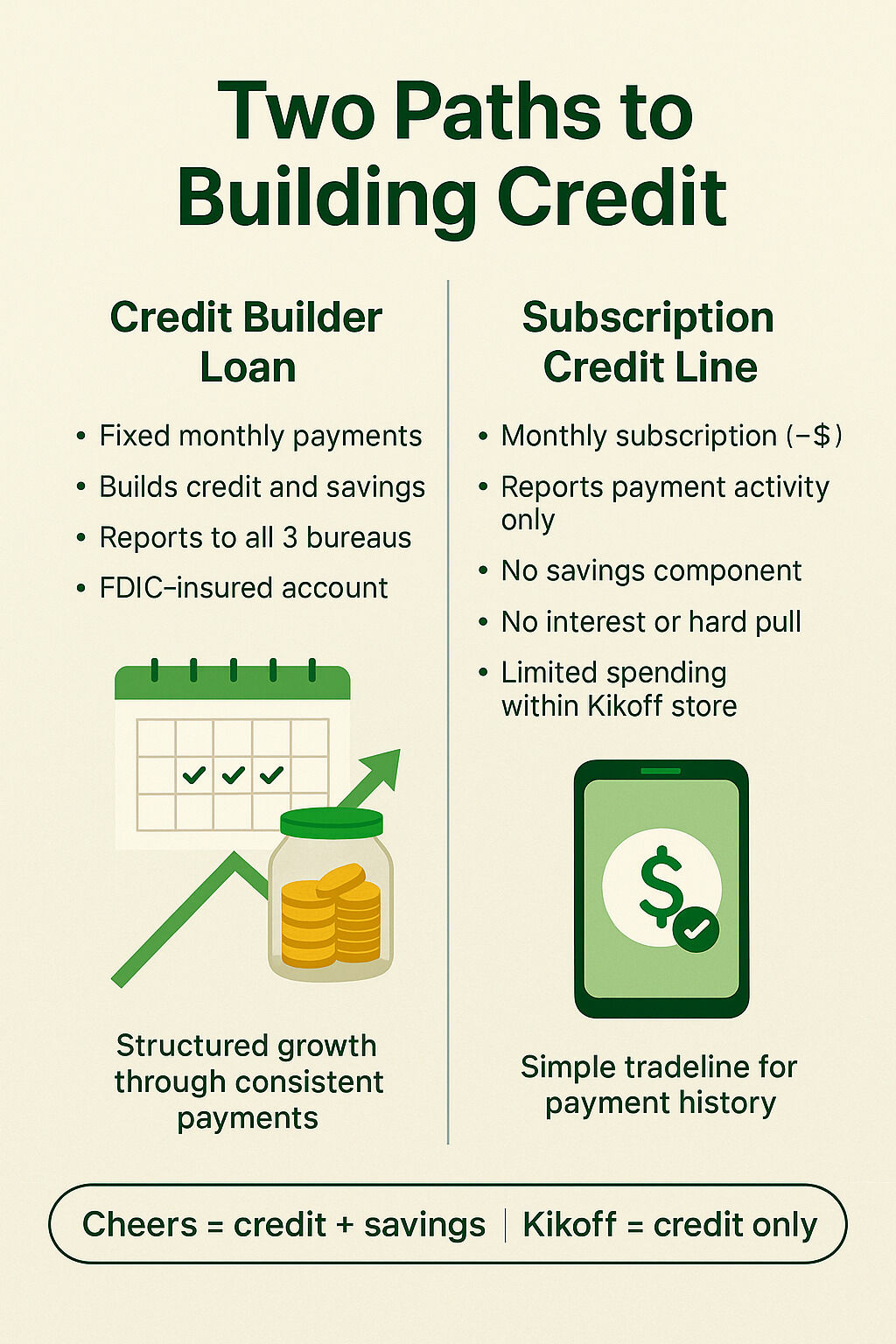

Building credit can feel like learning a new language. There are many tools-credit cards, loans, and apps- that promise to help, but it's not always clear how they actually work. Two popular options, Cheers and Kikoff, both claim to make credit building simple, yet they do it in entirely different ways.

One helps you build credit while saving money through fixed monthly payments. The other uses a revolving line of credit to report your payment activity. Understanding how each approach affects your credit profile can help you choose the one that fits your goals and budget.

Let's take a closer look at how Cheers and Kikoff work, what makes them different, and how each can help you start building positive credit history.

What Is Cheers Credit Builder?

Cheers Credit Builder is a credit-builder loan designed to make credit building automatic. When you open an account, you select a repayment plan that fits your budget, ranging from $528 to $3,168 over 24 months¹. Each month, you make a fixed payment plus a small interest. There are no administration or membership fees. Cheers reports every on-time payment to all three credit bureaus: Experian, Equifax, and TransUnion².

That reporting helps build your payment history, which makes up about 35% of your credit score, and adds variety to your credit mix³. Because Cheers is an installment-style account, it can strengthen two key scoring factors at once.

What Is a Credit Builder Loan?

A credit builder loan is designed to help people establish a credit history by making small, consistent payments over time. Unlike traditional loans, you don't receive the money up front. Instead, your monthly payments are held in a secure savings account while your progress is reported to the credit bureaus.

Each payment you make shows lenders that you can manage debt responsibly, which can help strengthen your payment history and overall credit profile. Once the loan term ends, you receive back the money you've paid, minus interest, giving you both credit growth and savings to show for it.

The funds you pay go into an FDIC-insured savings account held by Cheers's partner bank. Once you complete the term, you receive back the total amount you've paid, minus the interest⁴. You're not borrowing money to spend-you're building a track record of responsible payments while saving at the same time.

To understand how simple steps can help shape your credit, check out 7 Smart Ways to Build Credit in 2025.

What Is Kikoff and How Does It Work?

Kikoff takes a different approach to credit building than traditional installment products. Instead of lending you money to repay over time, Kikoff offers a revolving credit line, usually around $750-that's explicitly designed for building credit, not for everyday spending. You can only use it within the Kikoff Store to make small purchases, and every payment you make toward those purchases is reported to the credit bureaus.

Kikoff works on a subscription model that starts around $5 per month. That fee gives you access to the credit line and helps keep the account active while reporting continues. Because it reports to the major credit bureaus-Experian, Equifax, and TransUnion- it can help establish a history of on-time payments and improve your credit utilization ratio when managed responsibly.

There's no hard credit check, no interest charges, and no late fees in most cases. However, unlike Cheers, Kikoff doesn't return any of the money you pay at the end of your term. Its goal is to create a simple, low-cost way to add an active tradeline to your credit report, but it doesn't include a savings component.

For more details on how Kikoff's revolving credit line works, visit Build credit with a Kikoff Credit Account.

How Cheers and Kikoff Compare

Both Cheers and Kikoff report payments to the major credit bureaus, but how they help your score differs. Cheers is an installment account, meaning you commit to a fixed loan amount and make regular payments until the balance is paid off. This helps establish both payment history and credit mix. Kikoff, on the other hand, is a revolving account that stays open as long as you maintain the subscription.

When it comes to costs, Cheers only charges 12.15% APR and nothing else⁵. Kikoff's model is fee-based, meaning you pay a monthly subscription fee whether or not you make purchases.

At the end of the term, Cheers customers receive their savings back, giving them a tangible return on their effort⁴. Kikoff customers don't receive a payout; the benefit comes only from the account reporting.

Availability also differs. Cheers operates in all 50 states and D.C., while some Kikoff services vary by region or state. Both report quickly, but Cheers' first payment processes the next business day-often speeding up the credit reporting timeline compared to other builder loans that take a whole month before reporting begins⁶.

Which One Fits Your Credit Goals?

Choosing between Cheers and Kikoff depends on what kind of credit foundation you're trying to build. Both report to the major credit bureaus, but the way they help you grow credit looks very different.

If your goal is to build payment history while saving money at the same time, Cheers gives you a structure that rewards consistency. Each monthly payment not only helps strengthen your credit profile but also contributes to your savings. By the end of the loan term, you've built both a positive credit record and a small financial cushion-two things that can support long-term stability.

Kikoff can make sense for someone who wants a low-cost tradeline to start building history. Its revolving structure is easy to manage, but because you're paying a monthly fee instead of contributing to savings, the progress you make is tied entirely to on-time payments rather than financial growth.

Think about what matters most to you: immediate credit reporting or developing stronger money habits over time. If you want a deeper look at the habits that can strengthen your overall financial health, explore How to Build Credit in 2025 for practical strategies that complement whichever credit builder you choose.

Why Cheers May Be the Better Long-Term Option

Cheers focuses on sustainable credit building. It's built for people who want to grow their credit and their savings at the same time, without extra fees or confusion⁴. Reporting begins as soon as your first payment clears, giving you faster visibility across all three credit bureaus⁶.

Since your payments are automatically reported and stored in a secure FDIC account, every step contributes to your financial progress. Over time, this creates a consistent positive history and measurable savings-a combination few competitors offer.

Cheers welcomes everyone, including immigrants and newcomers to credit, and requires only an ID match to get started-no credit check, no hidden fees, and no barriers.

The Takeaway

Both Cheers and Kikoff were created to help people take control of their credit, but they take different paths to get there. Kikoff gives users a revolving tradeline that focuses only on payment history. It can help build a foundation for those who want a quick start, but it stops short of helping you save or create long-term habits.

Cheers, on the other hand, turns the process into something automatic. With a fixed plan, transparent pricing, and reporting to all three major credit bureaus, every payment you make builds credit and savings at the same time. By the end of the term, you don't just have better credit-you also have money set aside, which gives you a stronger financial base for whatever comes next.

At Cheers, the goal isn't just to raise a number-it's to make credit building simple, accessible, and sustainable for everyone. That's why there are no hidden fees, no hard credit checks, and no extra barriers-just a straightforward way to grow your credit and your confidence, one payment at a time.

Cheers is not a bank. Deposit accounts are held by Sunrise Banks, N.A. Member FDIC⁷.

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

References

• Kikoff - https://kikoff.com/credit-account

¹ Credit Builder Account Plans:

All plan options include a 24-month term, 25 total payments and a 12.15% Annual Percentage Rate (APR).

Plan A: Total Payments of $600 with $532.70 Amount Financed. $24 Monthly Payments and $67.30 Total Interest.

Plan B: Total Payments of $825.02 with $733.13 Amount Financed. $33 Monthly Payments and $91.89 Total Interest.

Plan C: Total Payments of $1,149.98 with $1,021.69 Amount Financed. $46 Monthly Payments and $128.29 Total Interest.

Plan D: Total Payments of $3,600.00 with $3,197.82 Amount Financed. $144 Monthly Payments and $402.18 Total Interest.

² Payment activity:

All payment activity is reported to the credit bureaus. On-time payments may help build your credit, while late or missed payments may negatively impact it. Results are not guaranteed and depend on your individual financial behavior and credit profile.

³ FICO® Credit Factors:

According to FICO®, 35% of your credit score is based on payment history, and 10% is based on credit mix. Cheers reports every payment and adds a secured installment loan to your profile. Source: myFICO - https://www.myfico.com/credit-education/whats-in-your-credit-score

⁴ Cancel Anytime & Get Savings Back:

At the end of your term, your total savings (minus interest) is returned to you. You can cancel your account at any time without penalty.

⁵ No Hidden Fees:

There are no application fees, maintenance fees, or early cancellation penalties.

⁶ Accelerated Reporting:

Accelerated reporting applies to the opening of your account, plus the first payment. Credit bureau reporting occurs monthly thereafter.

⁷ Cheers Disclosure:

Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval.

.png)