Asking yourself, "How many categories should you have in your budget?" is a reasonable question when trying to determine your overall budget. What seems like a complicated puzzle can be simmered down into a few pieces, where it's generally pretty easy to find where your money is going. In this article, we explore some ideas for budgeting. We’ll walk through why category overload hurts more than helps, the most popular budgeting models people are using in 2025, and how digital spending habits are reshaping how we budget. You’ll learn how loud budgeting is shifting social norms, what a practical category layout looks like, and exactly how to get started—even if you’ve never budgeted before. And if building credit is on your radar, we’ll show you how Cheers can support your goals while you organize your money.

Why Category Overload Can Hurt More Than Help

Too many categories can make your budget harder to follow. You get lost in the weeds trying to remember if Spotify goes under “Entertainment,” “Subscriptions,” or “Tech.” Every budgeting tool or influencer has their labeling system—but your budget isn’t supposed to impress anyone. It’s supposed to work.

On the other hand, having too few categories can blur the line between overspending and staying on track. If you lump takeout, grocery runs, and convenience snacks into one “Food” category, you’ll have no idea how much you’re spending on restaurants. And that’s when financial leaks begin to add up.

A bloated or vague budget makes it easier to miss patterns—and harder to make course corrections.

The Budgeting Models Most People Are Using in 2025

If you’re looking for structure, start with a ratio-based framework. These models help you define the types of categories you need—then you can decide how granular to get from there.

- 50/30/20 Rule: Allocate 50% of your income to needs, 30% to wants, and 20% to savings or debt. You can break each of these into smaller categories if needed.

- 60/30/10 Rule: A newer variation with more room for essentials—ideal if your fixed expenses take up more of your paycheck.

- 75/15/10 Rule: Emphasizes necessities and long-term growth. Popular among families and people navigating high inflation.

These aren’t category lists—they’re category types. They guide the shape of your budget and show you where to focus your attention.

So, How Many Categories Should You Have in Your Budget?

There’s no perfect number, but a good starting point is with 5 to 10 categories. Start with broad categories, including rent, groceries, transportation, and debt or savings. Keeping things manageable without losing the goal, you can track your spending on broad categories to see where you're overspending. However, if a category is too broad, like "food," consider splitting it into groceries and take-out. On the other hand, if you have infrequent spending- consider merging them into one category, where you don't need to worry about that granular category (as you don't need to consider its effect on your budget). It's essential to remember that your budgets should change with your needs. A solid budget encompasses the means of your lifestyle with your goals, and your blind spots should be covered.

Digital Spending Is Changing the Way We Budget

Budgeting in 2025 means more people are going cashless. That sounds convenient, but research shows swiping a card or tapping your phone makes it easier to overspend. It’s called the “cashless effect”—your brain doesn’t feel the pain of spending digital money the same way it does with cash.

This is where categories become even more helpful.

By clearly labeling where your money is going, you create artificial speed bumps before impulse purchases. You can set up digital “envelopes” for each category using a budgeting app or prepaid cards. Once a category runs out, you stop spending in that area—just like with physical cash.

What Loud Budgeters Are Doing Differently

There’s a movement this year called loud budgeting—the idea that you should talk openly about your money limits. If your friends are making weekend plans and you say, “That’s not in my fun budget this month,” you’re not being cheap. You’re being intentional.

But loud budgeting only works if your budget categories reflect your actual lifestyle. Don’t just budget for rent and bills. Include date nights, self-care, and vacations—even if you’re only putting $5 toward them right now. The goal is to be real, not restrictive.

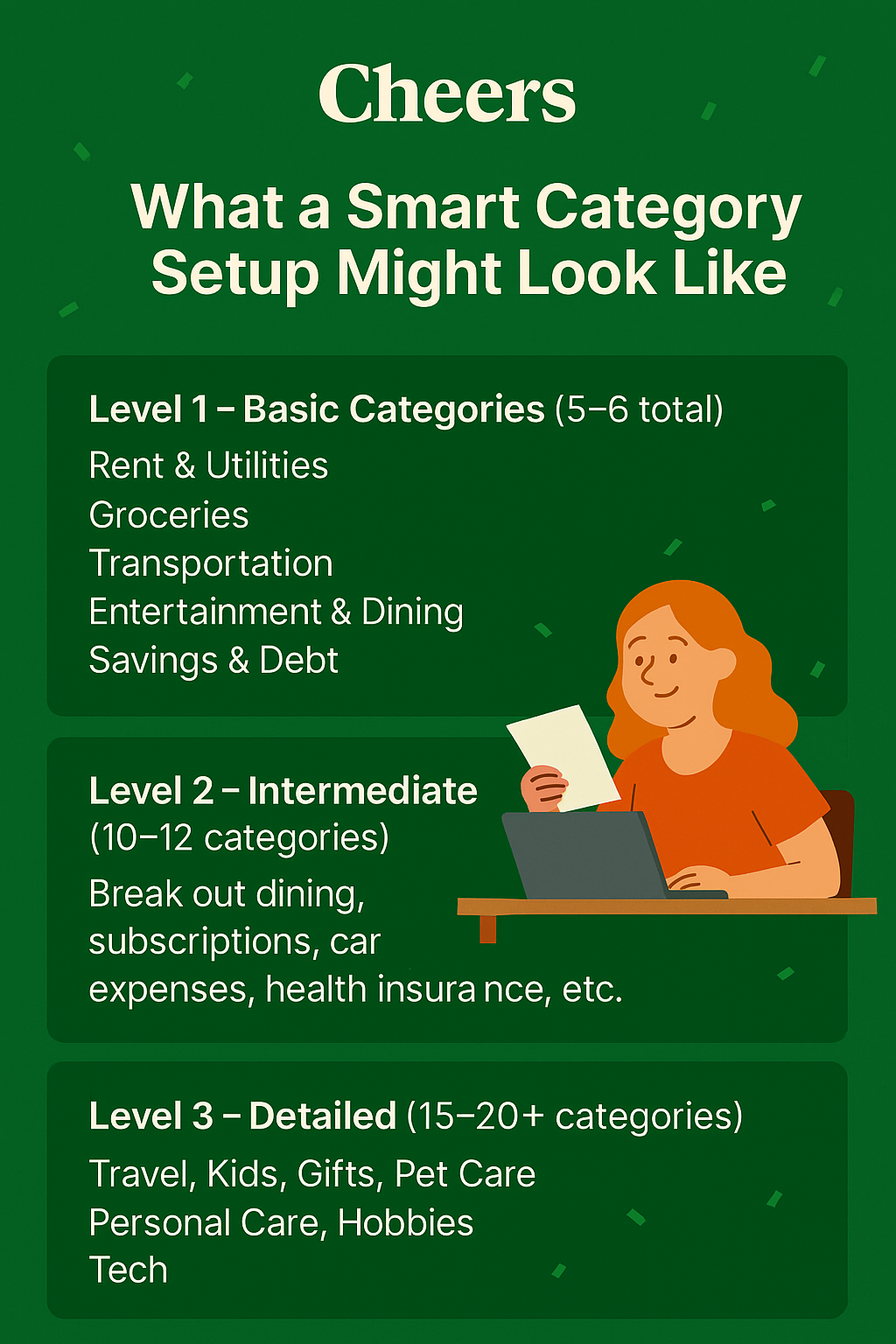

What a Smart Category Setup Might Look Like

Still not sure where to begin? Here’s a realistic setup that works for many people:

Level 1 – Basic Categories (5–6 total)

- Rent & Utilities

- Groceries

- Transportation

- Entertainment & Dining

- Savings & Debt

Level 2 – Intermediate (10–12 categories)

Break out dining, subscriptions, car expenses, health insurance, and other expenses.

Level 3 – Detailed (15–20+ categories)

Create line items for travel, children, gifts, pet care, personal care, hobbies, technology, and more. You can always grow into the more detailed setup. But don’t start there if it overwhelms you.

What to Do Right Now

Begin by reviewing your spending from the past month and categorizing it into five or six groups. That’s usually enough to spot habits and problem areas. From there, identify areas where you need more visibility—are you overspending on takeout, or unsure how much you’re allocating toward subscriptions? Break those out as needed. Don’t aim for perfection. Just aim for progress. A budget is a tool, not a test. The only fundamental mistake is building a budget you won’t use. Set a reminder to review your categories every couple of weeks, and allow yourself to update as needed.

Build Credit While You Budget Smarter

Cheers believes that building credit should be part of every smart budget. That’s why Cheers is a credit builder loan that reports your monthly payment activities¹ to all three credit bureaus—while the money you pay is securely held in a Certificate of Deposit (CD).

You choose your plan. You set your terms. You start building payment history right away, even if you’ve never had credit before. No hidden fees². No credit check.

If you’re working to get organized with your spending, Cheers fits right into your plan—just add it to your “credit building” category.

Final Thought: It’s Not About How Many—It’s About What Works

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

There’s no magic number of budget categories. Start simple. Track what matters. Add detail only when it clarifies things. The best budget is one you’ll stick to.

And if you’re ready to pair better budgeting with better credit, get started with Cheers.

(The opinions expressed in this article are the author’s own and do not reflect the view of Sunrise Banks³.)

1 Payment activity:

All payment activity is reported to the credit bureaus. On-time payments may help build your credit, while late or missed payments may negatively impact it. Results are not guaranteed and depend on your individual financial behavior and credit profile.

² No Hidden Fees:

There are no application fees, maintenance fees, or early cancellation penalties.

³ Sunrise Banks:

Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval. Must be at least 18 years old, have a valid U.S. bank account, and a Social Security Number.

.png)