When two people decide to build a life together, money becomes more than just a personal matter-it becomes a shared responsibility. Budgeting for couples means learning how to balance habits, values, and long-term goals without letting money become a source of stress. This article breaks down budgeting for couples, exploring options that work for partners, and how to handle differing incomes and build credit. Committing to your partner involves taking practical steps to build trust through complete transparency, which, in turn, fosters financial momentum. Plus, you'll see how tools like Cheers Credit Builder can help you strengthen your credit while saving toward your future as a couple.

Why Couples Struggle With Budgeting (And What You Can Do About It)

Budgeting tension usually has little to do with numbers. It's more about how each person thinks about money, what they were taught growing up, and what their expectations are now. Without complete transparency and a willingness to collaborate, omitting financial information and unspoken spending habits can lead to a disconnect in partnership. Sometimes, with different priorities- one couple wants to save and the other wants to spend lavishly on experiences.

The way forward isn't about forcing sameness - it's about creating understanding. Couples who succeed with budgeting tend to set clear expectations, use systems that feel fair to both partners, and commit to regular money check-ins. When you remove judgment and replace it with a shared plan, budgeting becomes less about control and more about teamwork.

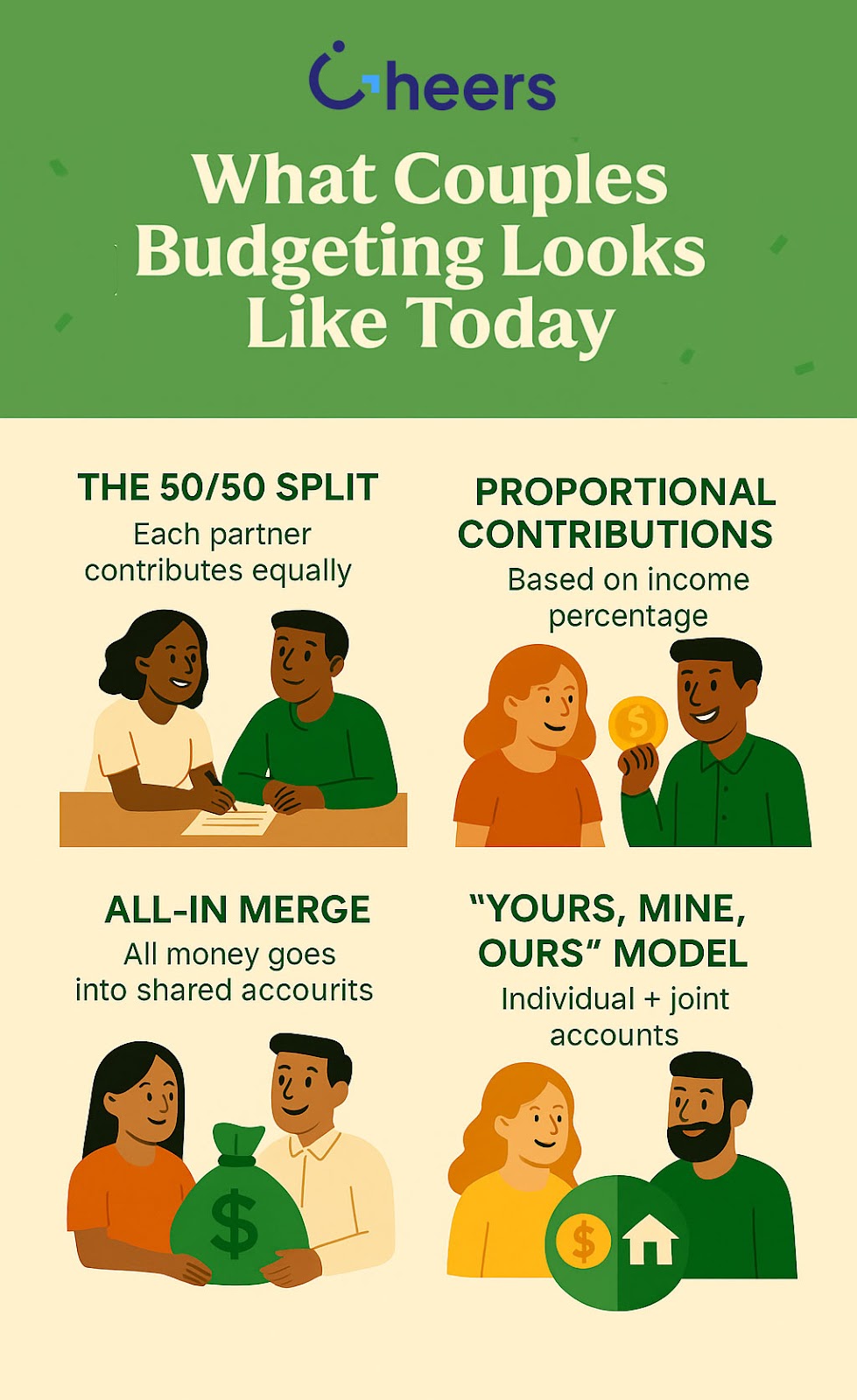

What Couples Budgeting Looks Like Today

Traditionally, couples would get married before going through a joint venture. However, nowadays, many couples share finances sooner, whether due to growing families or other circumstances. On the other hand, others keep their accounts separate well into the marriage. There is no right way; it depends on personal preferences. A hybrid model that keeps everyone's preferences can strike a balance and keep partners happy with their accommodations.

A few common approaches:

- The 50/50 Split: Preferred when both partners make a similar income, each partner contributes equally.

- Proportional Contributions: Partners contribute based on their income percentage, which is helpful when one earns more.

- All-In Merge: All funds are deposited into a single shared account. Often used in marriages or long-term partnerships.

- The "Yours, Mine, Ours" Model: Each person has individual accounts plus one joint account for shared expenses.

What's key is agreeing on how much goes into the shared pot, who tracks the bills, and how you'll make spending decisions together.

How to Start Budgeting Together Without the Tension

Budgeting for couples shouldn't feel tedious, and working together towards shared goals should be the primary objective. Complete transparency garners trust and is the cornerstone of a successful partnership.

Here's a roadmap that works:

Get Everything on the Table

List every source of income, everyday expenses, and savings goals. This may be uncomfortable at first, especially if one of you is dealing with credit card debt or student loans, but complete transparency is essential.

Choose a Budgeting Style That Fits Your Relationship

No rule says you need to merge all your finances. The best budget for couples is one that reflects how you already function as a team. Do you split dinner in half? Are you already paying different portions of rent based on income? Start there.

Set a Monthly Money Date

Put a recurring check-in on the calendar. Keep it low-stress. Go over upcoming bills, surprise expenses, and progress toward goals. Apps like YNAB or Monarch Money can help you visualize your cash flow together.

Define Shared Goals

Whether it's a vacation, a home, or paying off a car, shared goals keep both people motivated. Tie savings plans to those goals, not just abstract numbers—one powerful motivator: building credit together, so you can qualify for better rates and borrow smarter.

What About Debt, Credit, and Uneven Incomes?

Debt and credit can play a significant role in the dynamic of a relationship. Especially when one partner's income is significantly higher or the other partner is rebuilding their credit. As partnership goals may be inadvertently affected, it's essential to begin by being completely transparent about your current status. These discrepancies don't have to define the relationship, but it's critical to know the hurdles and roadmap for progress to achieve success. Student loans, credit card debt, and medical debt- they're all points to discuss with your partner to determine a sustainable roadmap together. If incomes are unequal, it's often more sustainable to split shared expenses proportionally.

For credit building, consider tools that help you move forward without taking on additional risk. Cheers Credit Builder allows you to set aside a manageable amount each month, which is reported to all three credit bureaus while being held in an FDIC-insured account. There's no hard credit check, and you get your savings back at the end, minus interest. This can be an excellent way for one or both partners to improve credit without borrowing or co-signing.

Budgeting Tips for New Couples vs. Long-Term Partners

If you've recently moved in together, starting with a low-commitment plan may be the best approach. A joint account for everyday expenses, such as rent and shared bills, is typically sufficient. By observing the costs for the next few months, partners can reassess new budgets.

For long-term partners or married couples, it's worthwhile to dig deeper. Talk about retirement contributions, credit goals, and how you'll save for future milestones. Whether you're buying a home or starting a family, your budget should reflect both your current situation and your plans.

Building Credit Together While You Budget

Credit can be a significant factor in major financial decisions, such as qualifying for a mortgage or auto loan. But instead of waiting until you need good credit, start building it now. Cheers Credit Builder gives couples a low-friction way to build credit while saving. You choose a monthly contribution amount that fits your budget. Payments are reported as on-time installment activity to all three credit bureaus, which can help improve your credit mix and payment history.

And because Cheers holds your payments in a savings account, you're not losing money to fees or unnecessary borrowing. It's a practical move for couples who are serious about building a financial future together, without incurring additional debt.

What to Do Right Now

If you're ready to take control of your finances together, begin by having an open conversation about what you both earn, owe, and want. Don't wait until a financial emergency forces the issue. Decide on a budgeting method that reflects your relationship-whether that's complete transparency, a shared account, or proportional contributions. View budgeting for couples as a flexible and growing model to fit your new needs. If one partner is building credit, consider Cheers.credit for a credit builder loan. A low-commitment and straightforward way to strengthen your credit profile, it's one less measure to worry about when budgeting for couples.

.png)