Author: Vince Adriatico (Ex-banker with 750+ Credit Score)

Date: 7/11/2025

You shouldn't feel uneasy when you check your bank account between rent, groceries, debt, and the occasional late-night fast-food run. Your money tends to vanish, and so you've tried budgeting apps, spreadsheets, and even stuffing cash in your sofa. None of it sticks. The real issue here isn't tracking dollars, it's not having a clear system for budget categories.

You Want Freedom, Not Just Another Budget

What most people want isn't just a budget-it's clarity. The ability to look at your money and instantly understand where it's going. To have control over your spending without constantly second-guessing yourself. That starts with setting up the right budget categories, built around your real life, not some rigid formula.

The Problem: Most Budgets Break Down Without a Simple Structure

If you've ever tried to stick to a budget and failed, you're not alone. The problem isn't discipline. It's that most budgeting advice skips a crucial step: organizing your money into clear, intentional categories. Without that, you don't know how much you should spend or save-until it's too late.

But when you break your money down into well-defined budget categories, you gain the clarity and confidence to make smarter decisions.

We've Done the Research. Here's the Plan.

At Cheers, we study how real people manage money and how small shifts in financial behavior can change everything. Here's how we guide people through setting up budget categories that work.

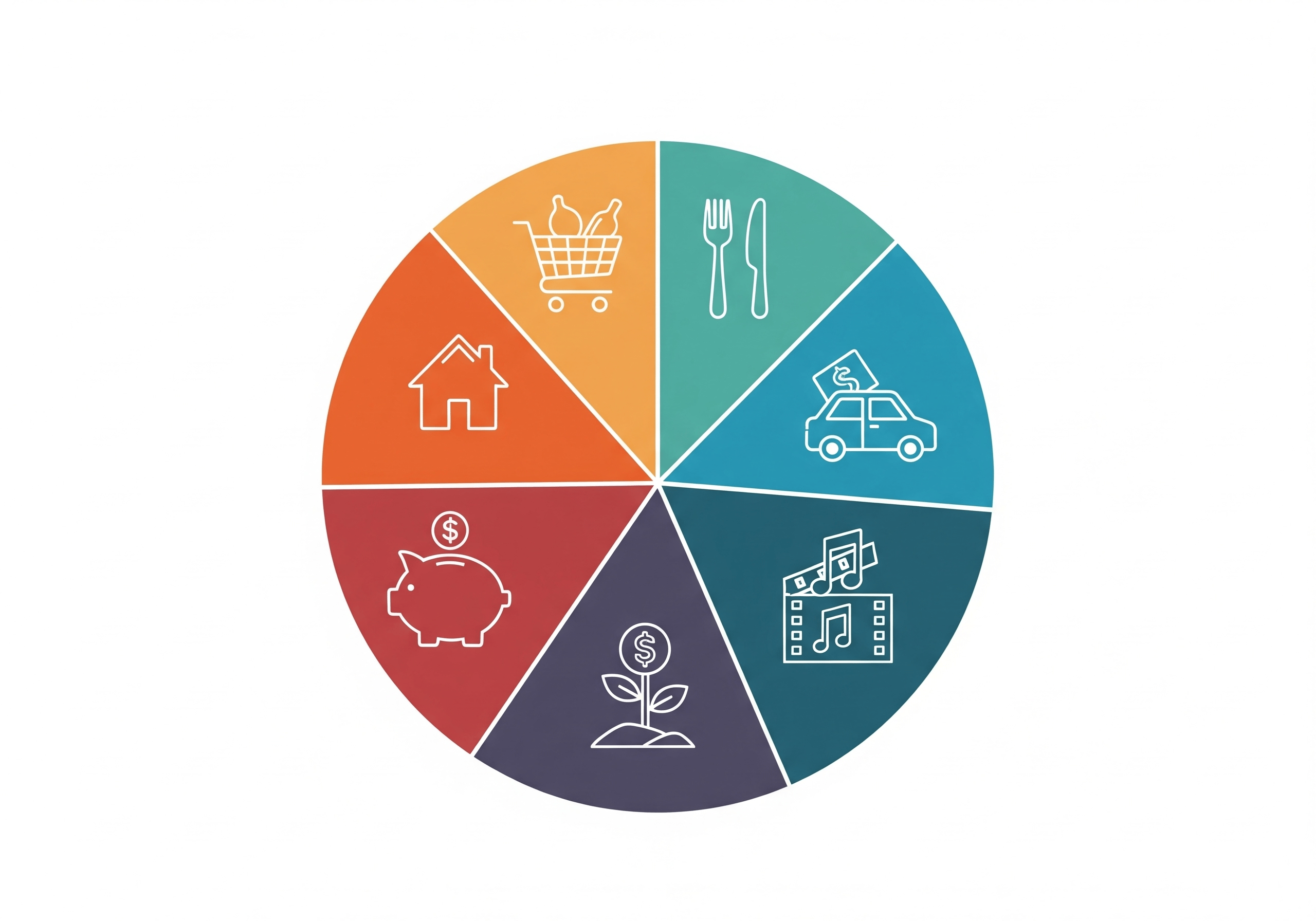

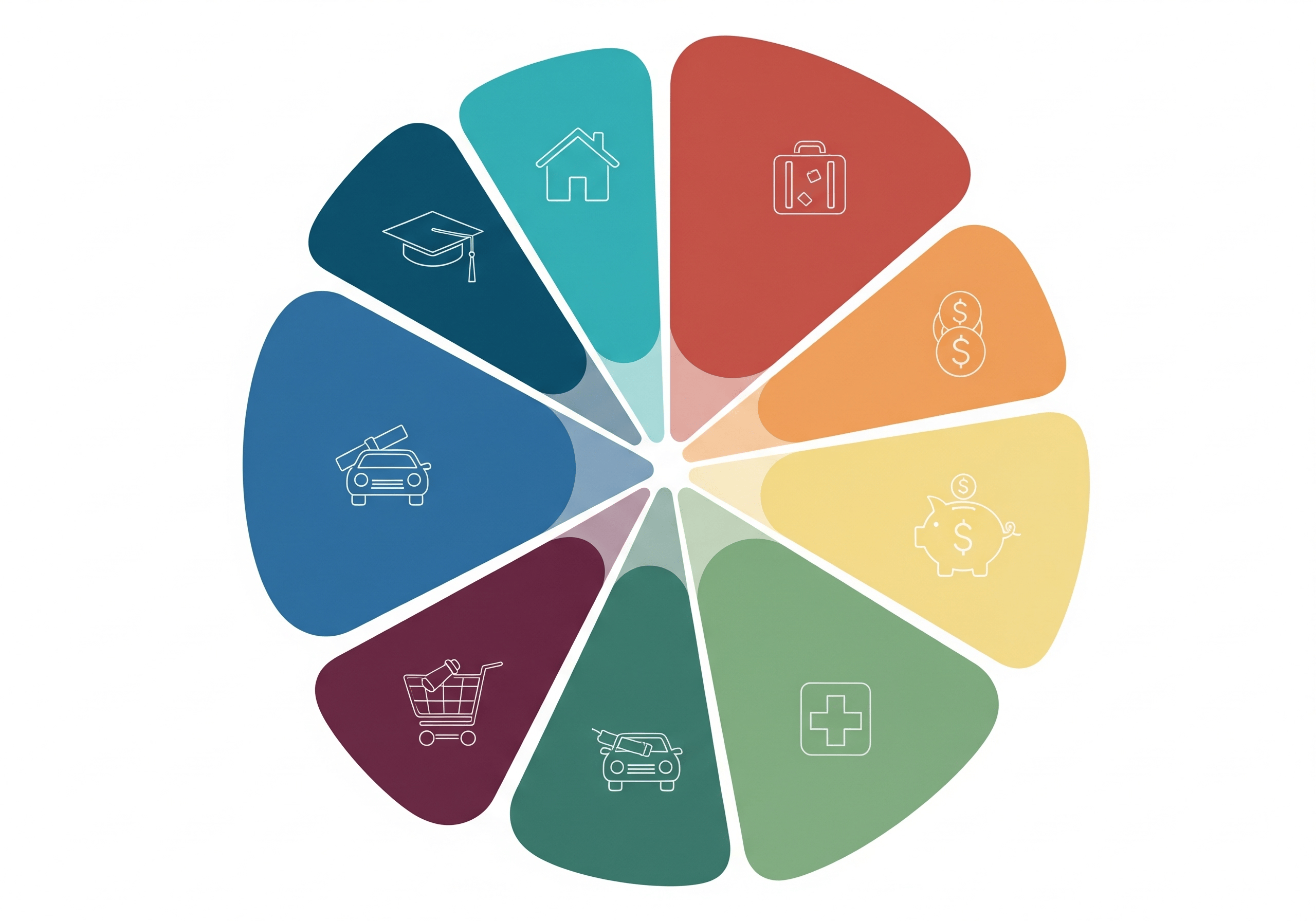

Step 1: Start With the Essential Budget Categories

Here are the budget categories you need to give every dollar a job:

- Housing - Rent, utilities, renters' insurance

- Food - Groceries, takeout, meal subscriptions

- Transportation - Gas, rideshares, insurance, maintenance

- Debt Payments - Credit cards, loans (use the debt snowball method for extra impact)

- Health & Personal Care - Prescriptions, doctor visits, gym

- Entertainment & Subscriptions - Streaming, events, hobbies

- Savings & Emergency Fund - Short-term, long-term, retirement

- Miscellaneous - Gifts, travel, pet care, unexpected expenses

- Cushion - A 3-5% buffer for the unknown (recommended by Self Inc)

This isn't about restriction. It's about giving every dollar a purpose so your money finally works for you, not the other way around.

Step 2: Use a Flexible Budgeting Rule That Fits Your Lifestyle

The classic 50/30/20 rule (needs/wants/savings) still works, but it's not the only way. Trending alternatives like:

- 75/15/10: Spend 75% on needs, invest 15%, save 10%

- 60/30/10: Lower your needs to 60% so you can spend more on wants

No one-size-fits-all ratio exists. Use the rule as a starting point, but adjust it to match your income, goals, and lifestyle.

Step 3: Create Momentum With the Debt Snowball

One of the most talked-about methods right now is the debt snowball: Pay off your smallest debts first, regardless of interest rate, to build motivation. It turns debt payments from an endless grind into a series of wins. You'll want to include this method in your budget categories so debt becomes a focused, strategic part of your plan.

Step 4: Don't Forget the Cushion Category

Other financial coaches stress the importance of a "cushion" category. Life is unpredictable. A 3-5% buffer can protect your budget from car repairs, vet visits, or last-minute flights. If you don't need it one month, roll it into savings or debt payments.

Step 5: Track, Adjust, and Stick With It

Your budget should grow as your priorities change. Checking your budget weekly, it's essential to update your budget categories as the flow of income changes. Got a raise? Maybe try to look into investments. Loss of a job? Look more into putting money into essentials. Flexible budget habits are significant as you go through the turbulations of life.

Imagine Your Budget Working

You wake up, check your account, and see that everything's in place. Rent is paid. Groceries are covered. A little is going into savings, and your credit score is on the rise because your payments are on time.

This is what happens when your money is organized into smart, custom-fit budget categories.

No more guessing. No more guilt. Just progress.

Want to Build Credit While You Budget?

Cheers Credit Builder can be the savings category in your new budget plan. It's not a credit card or a loan; it's a monthly payment you make that gets reported to all three credit bureaus, designed to build credit while you save. No hard pull. No setup fees. Just credit building on autopilot.

Start building credit with Cheers

Final Thought

When your budget has structure, everything gets easier. You don't need to be perfect-you need a plan. And it starts with building your list of budget categories that reflect your real life.

Don't let your money control you. Take the first step toward clarity, confidence, and a better financial future.

.png)