Financial management can feel overwhelming without a tried-and-true system; household budget categories may seem cumbersome. However, these household budget categories provide a structure to the system by organizing expenses into predetermined everyday needs. This article explores the concept of household budget categories, the trending methods people are using to manage them, a breakdown of the most common categories, and how to create a realistic budget using these categories. You'll also see how Cheers Credit Builder can fit naturally into your budget as a tool to help grow your credit while saving.

What Are Household Budget Categories?

Household budget categories are the buckets into which you sort your spending—housing, food, transportation, and so on. By grouping your expenses, you gain a clearer picture of where your money goes and how much is left for goals such as paying down debt, building savings, or improving your credit score.

They're the foundation of any working budget. Without them, every dollar feels like it's up for grabs.

Some people use just a few categories. Others break things down to the last detail. What matters is finding a structure that reflects your life-and sticking with it.

Budget Categories and Building Credit Go Hand in Hand

When you're trying to build credit, the way you manage your money every month plays a significant role. Looking beyond diligence with payments, household budget categories provide clarity on bills, which means you have less to worry about when all your bills are due at once. Tracking your spending across household budget categories, you can identify financial opportunities that can be allocated towards debt payments or tools like a credit builder loan. Similarly, it provides a chance to build your savings, which lenders typically consider a sign of financial responsibility. Within a budget system, it's easier to prioritize payments, which can help strengthen your credit, as well as give assurance that other miscellaneous bills are taken care of, such as utilities, phone bills, and recurring loans.

Trending Budgeting Approaches You Should Know

You're not alone if you've scrolled past a "Cash Stuffing" video on TikTok or heard about "Zero-Based Budgeting" but weren't sure what it meant. These trends are everywhere for a reason-they're helping people stick to a budget.

Cash Stuffing (a.k.a. Envelope Method)

This approach provides you with physical cash for categories such as groceries or gas. Once the envelope is empty, you're done spending. Gen Z has revived this method to fight back against digital overspending-and it's working.

Use it for categories where you tend to lose track, such as restaurants, entertainment, or personal care.

Zero-Based Budgeting

Every dollar has a job. Your income minus expenses equals zero. That doesn't mean you have nothing left-it means even savings and debt payments are assigned a spot. This method is powerful if you want to feel in control, not confused.

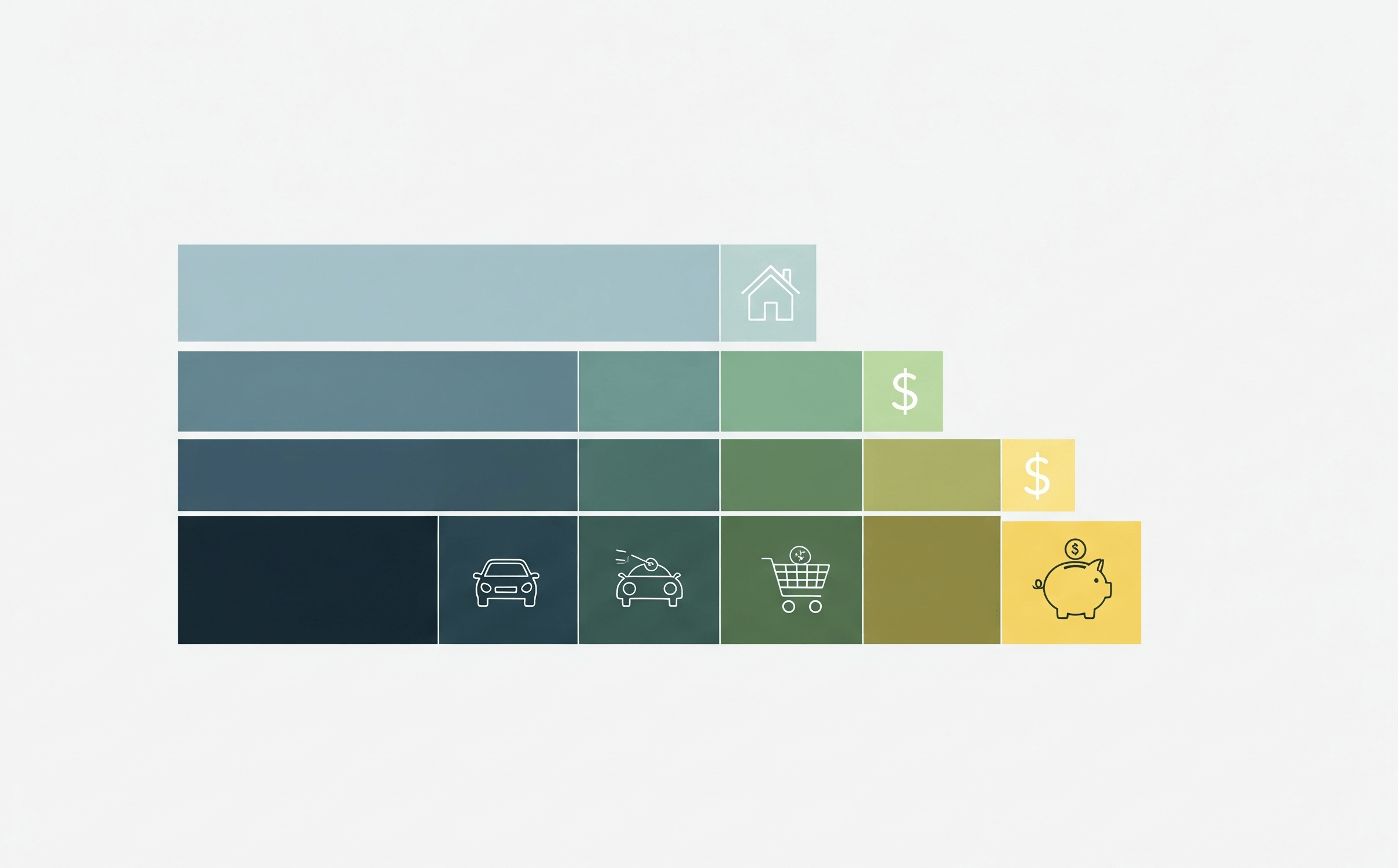

50/30/20 Rule (or Your Version of It)

A simple breakdown:

- 50% needs (housing, bills, food)

- 30% want (streaming, dining out)

- 20% savings and debt payoff

Can't make those numbers work right now? Many people adjust this framework to 60/20/20 or 70/10/20 depending on their income and cost of living.

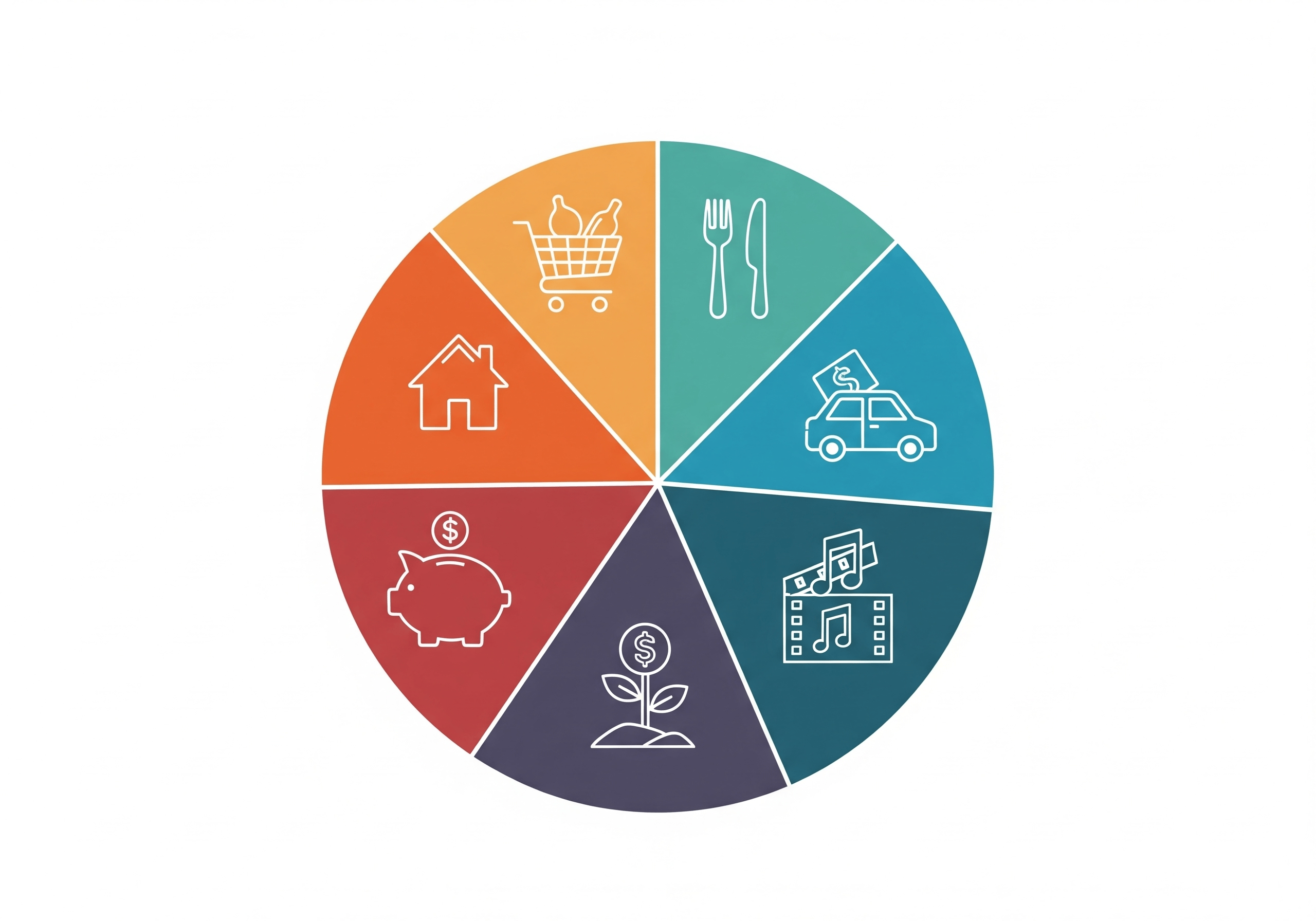

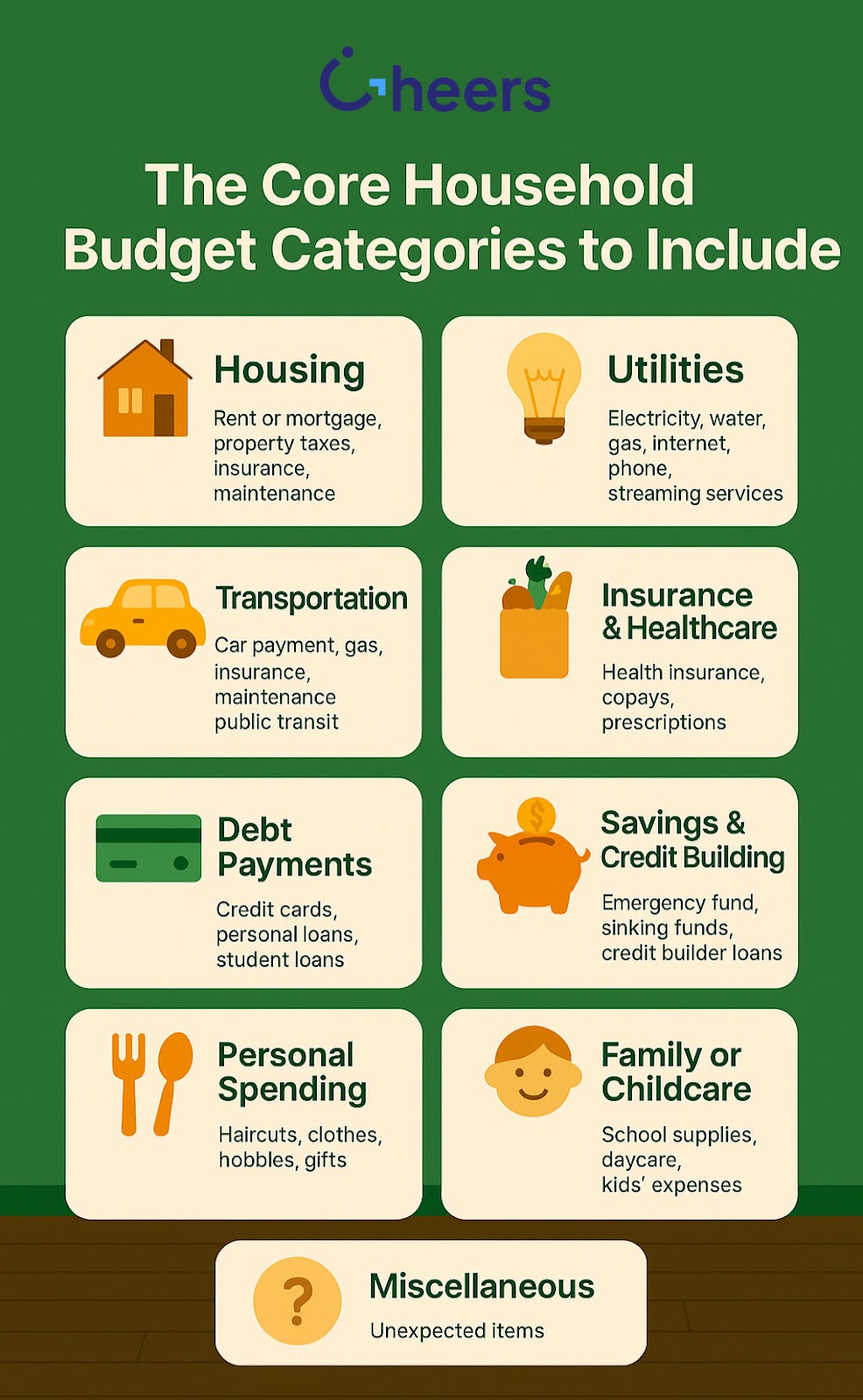

The Core Household Budget Categories to Include

You don't need a spreadsheet with 47 tabs. You need to know your main categories —and which ones require extra attention. Here's a structure to get started:

1. Housing

Rent or mortgage, property taxes, insurance, maintenance. This should be your priority. It's usually your most significant fixed expense and the most essential.

2. Utilities

Electricity, water, gas, internet, phone, and even streaming services. These are recurring and can be easily forgotten when they're on autopay.

3. Transportation

Car payments, gas, insurance, maintenance, public transit. Include parking if it's a regular expense.

4. Food

Groceries and takeout. Keep them separate if that helps you cut back more easily.

5. Insurance & Healthcare

Health insurance premiums, copays, prescriptions, dental visits, and over-the-counter meds. These add up fast-plan for them.

6. Debt Payments

Credit cards, personal loans, student loans. This is a must-track category if you're trying to improve your credit score.

7. Savings & Credit Building

Emergency fund, sinking funds (like holiday gifts or car repairs), and credit-building tools. This is where Cheers Credit Builder fits in. You set aside a fixed amount each month that builds your credit while also accumulating savings.

8. Personal Spending

Haircuts, clothes, gifts, hobbies, or anything that isn't a need but is still part of your lifestyle.

9. Family or Childcare

School supplies, daycare, kids' clothes, and medical needs. These are often overlooked and can throw off your monthly plan.

10. Miscellaneous

Because life is messy, leave room for those "oh no" moments-whether it's a broken faucet or a birthday you forgot was coming.

How to Build a Realistic Household Budget

A realistic budget starts with what you're spending, not what you wish you were paying. Look at the past two or three months of bank transactions and sort every dollar into a household budget category. This gives you a starting point. From there, you can identify areas that require limits, such as dining out or subscriptions, and make intentional decisions about what to cut or adjust. Use a method that fits your style-whether that's cash envelopes, an app, or a simple spreadsheet. Set goals for your flexible categories, automate bills and savings where possible, and check in every couple of weeks to see what needs to be adjusted. The goal isn't perfection-it's consistency.

How Cheers Can Help You Make the Most of Your Budget

If you're already working with budget categories, the next step is to add something that works with your financial goals, not against them.

Cheers Credit Builder fits perfectly into your "Savings & Credit" category. You choose a loan amount and term that works with your monthly budget. Your payments are reported to all three credit bureaus, and at the end of the term, you receive your money back, minus interest. There's no admin fee, no credit check, and your payments start helping your credit right away.

You're not taking on new debt. You're using what you've already budgeted to build a stronger credit profile and create a cushion for the future.

Your Next Step

Your money deserves direction, not just reaction. Whether you're paying down debt, trying to break the cycle of living paycheck to paycheck, or starting fresh in your credit journey, household budget categories are a key way to regain control.

Start by writing down your categories. Sort your recent expenses. See where your money is going. Then, plug in the missing piece, like Cheers Credit Builder, to turn your budget into a launchpad.

Want a step-by-step guide to setting up your categories or using Cheers to build credit while saving? Follow our blog to find the latest in budgeting, credit tips, and tools that work!

.png)