Your current balance is the real-time amount you owe on a credit account. This includes purchases, fees, interest, and payments that have been posted to your account. It changes as you use your card or make payments. You can check it by logging into your card issuer’s or lender’s app or website.

This number differs from your statement balance, which only includes transactions from the most recent billing cycle. Your current balance gives you a more up-to-date picture of your debt.

Current Balance vs. Statement Balance

Your statement balance reflects the amount due at the end of your most recent billing cycle. It stays the same until the cycle ends again. If you pay this amount by the due date, you usually avoid interest charges.

Your current balance, on the other hand, changes as you continue to use your card. Let’s say your statement balance is $400. Then, you make another $200 in purchases. Your current balance is now $600—even though you haven’t received a new statement yet.

The NerdWallet explains this difference and why it matters when you pay.

Why It Matters for Your Credit

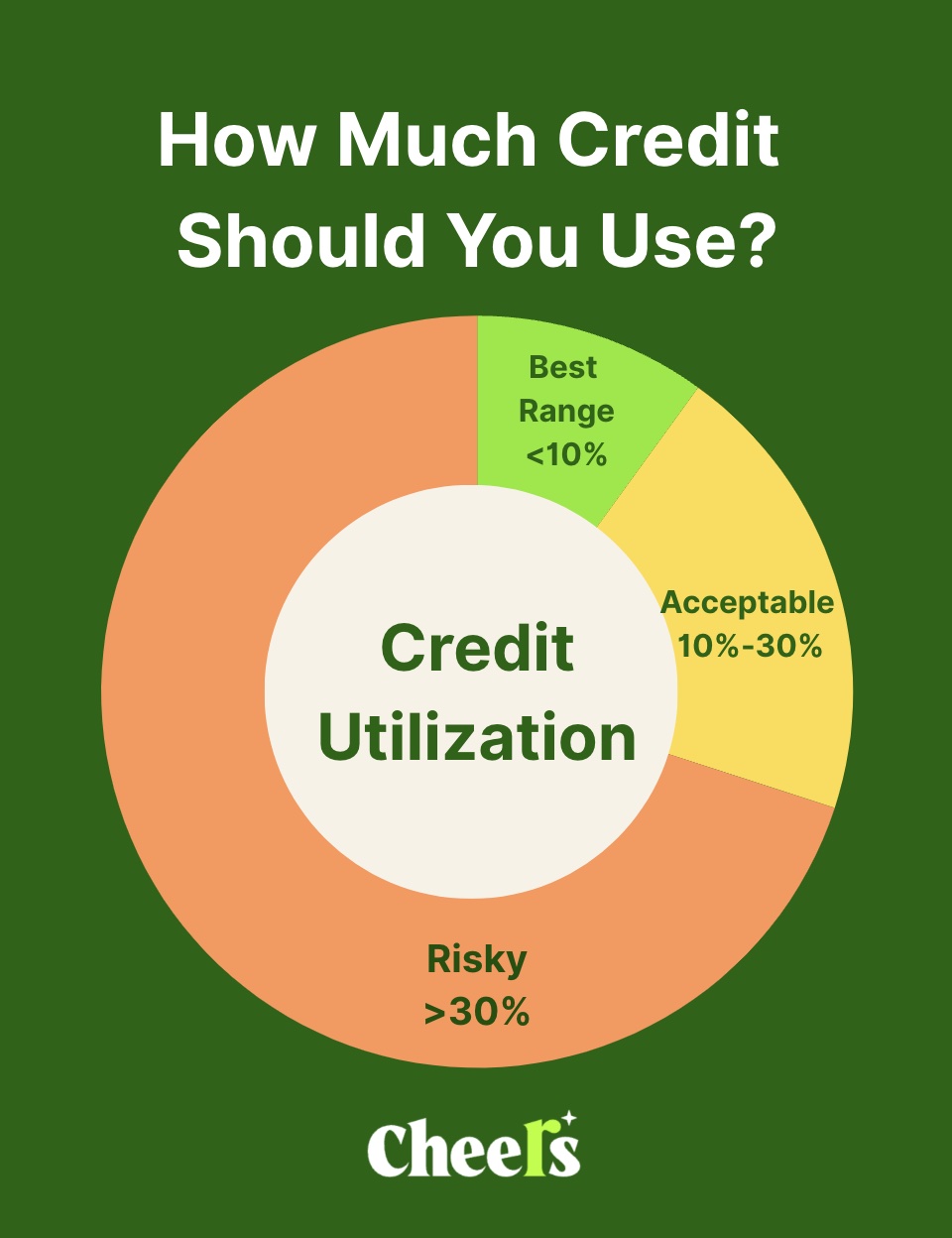

Even if you consistently pay off your statement balance, a high current balance could still affect your credit utilization ratio. That ratio compares your current balance to your total credit limit. A higher ratio may lower your credit score.

Let’s say you have a $1,000 limit and a current balance of $800. That’s 80% utilization—much higher than the recommended 30% threshold. Some credit scoring models look at your balance at the time it’s reported to the credit bureaus, not just when your statement closes.

Your current balance also matters on installment loans. On a loan, such as a credit-builder account, it shows how much principal is left. As you make monthly payments, your current balance drops—and if the lender reports on-time payments to the credit bureaus, your credit history gets stronger.

Managing Your Current Balance

There are easy ways to stay on top of your current balance:

- Pay early or multiple times a month. This lowers your balance before it gets reported.

- Set spending alerts. Most credit apps let you set balance thresholds.

- Know when your issuer reports. Some banks report your balance before the due date.

Tracking your current balance helps you stay below your credit limit and avoid unintentional dips in your score. It also helps prevent missed payments or over-limit fees.

If you’re new to credit, using an installment-style tool like Cheers Credit Builder lets you keep your balance predictable. There’s no temptation to overspend, and each payment moves you forward.

Common Issues and FAQs

Does the current balance include pending charges?

Usually, yes. Some banks include pending purchases in your displayed balance, but they’re not finalized yet. This is why your balance can feel higher than expected.

What happens if I overpay?

Overpaying your current balance can result in a negative balance. While this won’t hurt you, it also doesn’t improve your score. It just means your lender owes you money.

Can my current balance increase after I make a payment?

Yes, especially if you make more purchases before the payment posts. Your current balance is a live reflection of your account activity, not a final number.

How Cheers Helps You Build Credit

If you’re building credit from scratch or trying to rebuild it, keeping your current balance under control is key. Cheers Credit Builder is designed to help you do just that—without a credit card.

When you sign up, you choose a loan amount and a term that fits your budget. Your payments go into an FDIC-insured account. Each month, Cheers reports your payment to all three major credit bureaus. That helps establish a strong payment history, which makes up 35% of your credit score.

And because the loan is structured as an installment, your current balance will only go down. No surprises. No revolving debt. It's just consistent progress.

Want more credit tips like this?

Subscribe to our newsletter to get advice, tools, and updates from Cheers—your partner in building credit on autopilot.

References: