Ever wonder why your credit card shows both a statement balance and a current balance—and why they’re rarely the same? Understanding how each works is essential for managing your finances and establishing a strong credit history. Choosing the wrong one to pay could result in interest charges or a temporary decrease in your credit score. Let’s break it down.

Understanding Statement Balance

Your statement balance is the total amount you owed at the end of your last billing cycle. This includes all purchases, payments, and fees that were posted before the cycle closing. It doesn’t include any activity that happened afterward.

For example, if your billing cycle ended on May 31 and you spent $500, your statement balance would be $500. Any purchases made after that won’t appear on the following statement.

Paying the full statement balance by the due date avoids interest, thanks to a grace period offered by most cards. The Consumer Financial Protection Bureau (CFPB) confirms that paying the complete statement balance each month is the best way to keep your card interest-free.

What Current Balance Means

Your current balance is the total amount you owe at this time. This figure includes everything from your statement balance plus any new purchases, fees, or payments made since your last cycle ended.

If your statement balance is $400 and you buy $200 worth of groceries after the cycle ends, your current balance becomes $600. It keeps updating as you spend or make a payment.

You can find your current balance by logging into your bank or card provider’s app or website. While it reflects your up-to-the-minute account status, it can make budgeting tricky if you’re not watching closely.

Why the Balances Are Often Different

The difference between statement balance and current balance comes down to timing. Your statement balance is fixed once the billing cycle closes. Your current balance, on the other hand, keeps changing with every transaction.

This gap can be confusing. For example, you might think you’ve paid your card in full, only to see more charges appear the next day. That’s why understanding both is key to avoiding unnecessary fees or missed payments.

How They Impact Interest Charges

To avoid interest, always focus on paying the full statement balance by the due date. Even if your current balance is higher, you won’t owe interest on new charges as long as the statement balance is paid off and your card offers a grace period.

If you only pay the minimum or a partial amount, you lose the grace period and may start paying interest on every new purchase immediately. According to NerdWallet, this can lead to a growing balance even if you’re trying to stay on top of payments.

Which Balance Should You Pay?

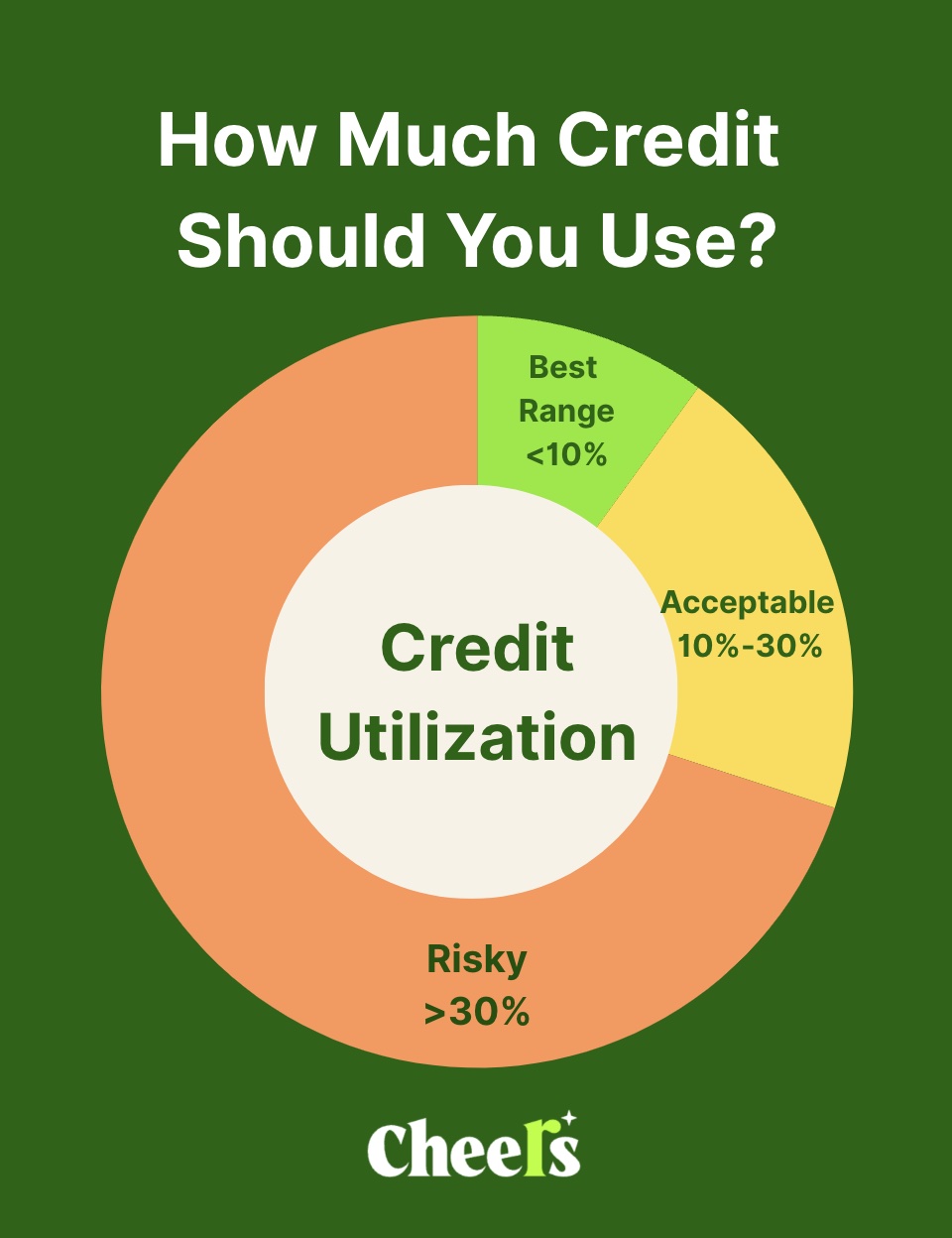

If your goal is to avoid interest, pay your statement balance in full each month. If you want to keep your credit utilization low, especially before making a significant financial move like applying for a loan or mortgage, consider paying down your current balance as well.

The Federal Reserve recommends keeping your utilization below 30%, but many credit experts suggest aiming for under 10% for better credit outcomes.

The Effect on Your Credit Score

Only the statement balance usually gets reported to the credit bureaus. So even if you pay down your card after the cycle ends, your credit report might still show a higher balance.

That can affect your credit utilization ratio, a key part of your credit score calculation. If you’re trying to boost your score, time your payments just before the statement closes so a lower balance gets reported. This strategy is especially helpful when working to rebuild or establish credit.

A Smarter Way to Build Credit with Cheers

If tracking your statement balance vs. current balance sounds overwhelming, Cheers offers a simpler path. The Cheers Credit Builder loan helps people build credit without needing to juggle credit cards. You set a plan and make monthly payments, and each payment gets reported to all three major credit bureaus.

Cheers charges no hidden fees—just a low 1% monthly APR—and helps you save money while building credit. It’s also faster than other credit builders because your first payment is reported the next business day after signing up. That means you can start seeing progress sooner.

Cheers is open to everyone, including immigrants and first-time credit users. There’s no hard credit pull, and it only takes a few minutes to get started.

Final Thoughts

Understanding the distinction between statement balance and current balance can help you maintain control over your finances and avoid common pitfalls. Whether you're paying off debt, monitoring your credit score, or trying to save money, it's helpful to be informed. And if you're ready to start building credit without the confusion, Cheers offers a smarter, low-stress way to do it.

References: