When you log in to your bank account, two numbers often appear: your available balance and your current balance. They might look similar, but they don’t mean the same thing. Confusing the two can lead to overdrafts, declined payments, or overspending beyond your actual balance.

Let’s break down what each balance really means and how understanding the difference can help you manage your money better.

What Is a Current Balance?

Your current balance is the total amount of money in your account based on all transactions that have fully cleared. This includes deposits and payments that the bank has already processed. It’s a running total, showing what you had at the start of the day, plus any settled activity.

However, this number doesn’t account for pending transactions. If you have made a purchase or have a bill payment pending processing, it won’t be reflected here yet.

What Is an Available Balance?

Your available balance is the amount you can actually spend or withdraw right now. It adjusts your current balance by subtracting anything on hold or still pending. So, if you used your debit card at the grocery store, that transaction reduces your available balance immediately—even if it hasn’t officially been posted yet.

This is the number that banks use to determine whether to approve a transaction. It’s also the balance that determines whether you’ll be charged an overdraft fee.

You can find a clear definition on Investopedia, which explains how financial institutions calculate available funds.

Why the Difference Matters

Let’s say your current balance is $1,000, but you have a $400 rent payment that hasn’t posted yet. Your available balance would show $600. If you try to spend more than $600, your transaction could be declined or cause an overdraft.

Many people make financial decisions based on the current balance because it looks like more money is available. But your available balance is the real indicator of what you can spend.

Especially during weekends or holidays, delays in processing can create bigger gaps between the two balances. Some businesses also place temporary holds for more than the actual charge—hotels, gas stations, and car rentals are common examples.

How This Affects Overdrafts and Pending Transactions

Overdraft fees are often triggered when someone spends based on their current balance rather than their available balance. According to Bankrate, the average overdraft fee is about $30 per transaction.

If a transaction is pending, that money is already “spoken for.” Even if the transaction hasn’t cleared, your available balance reflects that subtraction. If you’re not watching closely, it’s easy to overspend.

Also, keep in mind that banks may reorder transactions, which could result in more overdraft fees than you expect. That’s another reason why tracking your available balance vs current balance is essential.

Tips to Stay in Control of Your Account

- Always check your available balance before making purchases.

- Use your bank’s mobile app to get real-time balance updates.

- Set up low-balance alerts to avoid overdrafts.

- Understand how long it takes for deposits to clear—especially checks.

- Leave a buffer in your account to absorb any unexpected holds.

Even a small misunderstanding of your available balance can result in significant fees. Make it a habit to check both balances and determine which one to trust before you make a purchase.

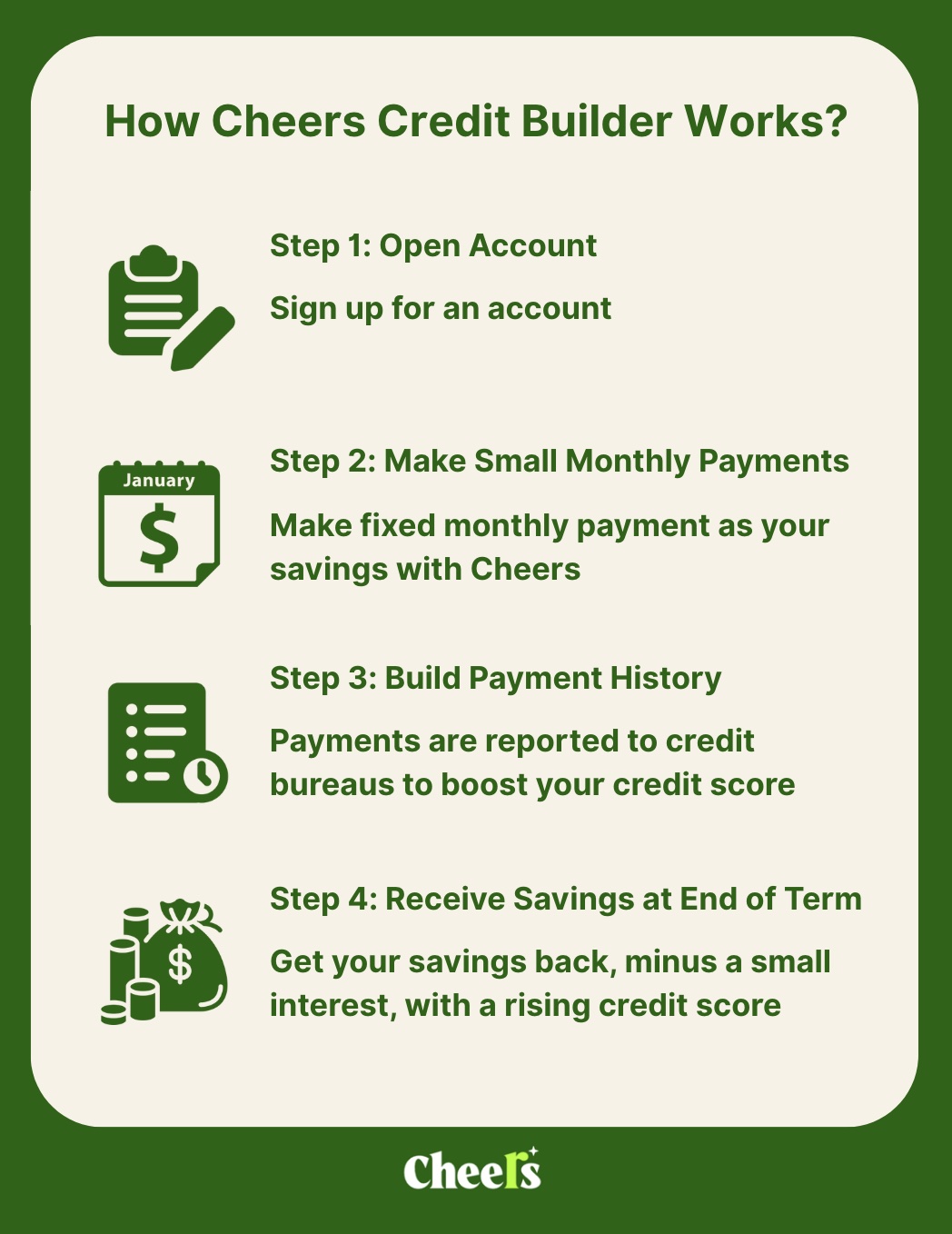

How Cheers Helps You Build Financial Confidence

Understanding the difference between available balance and current balance helps you avoid fees and manage your finances more effectively. But if you’re working to improve your credit, just tracking your bank account isn’t enough.

That’s where Cheers Credit Builder can help. It’s a simple way to build credit without using a credit card. With no admin or membership fees, Cheers only charges a low monthly APR. Your payments are reported to all three credit bureaus, which helps build a positive payment history and improve your credit mix.

The best part? You get your payments back at the end of the term, minus interest. That means you're building savings and credit at the same time. Cheers is fast to report—your credit building starts the day after you sign up.

If you're looking for a stress-free way to improve your credit while growing smart financial habits, learn more about Cheers Credit Builder.

References