Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 6/8/2025

Table of Contents

- What Is a Secured Card?

- How Secured Cards Work

- Pros and Cons of Using a Secured Card

- How a Secured Card Helps Build Credit

- Secured Cards vs. Credit Builder Loans

- Getting Started with Cheers

What Is a Secured Card?

A secured card is a type of credit card that’s backed by a refundable deposit. That deposit acts as collateral and usually sets your credit limit. If you deposit $300, your card’s limit will typically be $300. Secured cards are often recommended for people with poor credit or no credit at all.

They can help you build credit by reporting your monthly payment activity to the credit bureaus. Over time, responsible use may improve your credit score and lead to approval for an unsecured card. According to Experian, secured cards are one of the most common ways people start building a credit history.

How Secured Cards Work

To open a secured card, you apply like you would with a regular card. Some issuers check your credit, while others may not. Once approved, you fund the card with a deposit. That deposit stays in the account as a safety net for the lender. You can then use the card for purchases and make monthly payments.

Each payment you make is reported to credit bureaus—Experian, Equifax, and TransUnion. Late or missed payments can hurt your credit, while on-time payments help build a positive credit history.

Pros and Cons of Using a Secured Card

The most significant benefit of a secured card is the access it provides. You don’t need great credit to qualify, and in many cases, there’s no hard pull on your report. Some issuers will upgrade your account to an unsecured card after several months of responsible use and refund your deposit.

But secured cards come with some downsides. Many charge annual fees, have high interest rates or limit you to very low credit lines. The upfront deposit may also be hard for some to afford. Therefore, it’s essential to understand all the fees and terms before applying.

How a Secured Card Helps Build Credit

A secured card builds credit through regular reporting to the credit bureaus. If you make on-time payments and keep your balance low, your credit score may improve over time. The most important factor in your credit score is payment history, which makes up about 35% of your score.

Using a secured card responsibly shows lenders that you can handle borrowed money. After 6 to 12 months of good behavior, some issuers will offer you an unsecured card. But make sure your card issuer actually reports to all three credit bureaus—some smaller issuers may only report to one.

Secured Cards vs. Credit Builder Loans

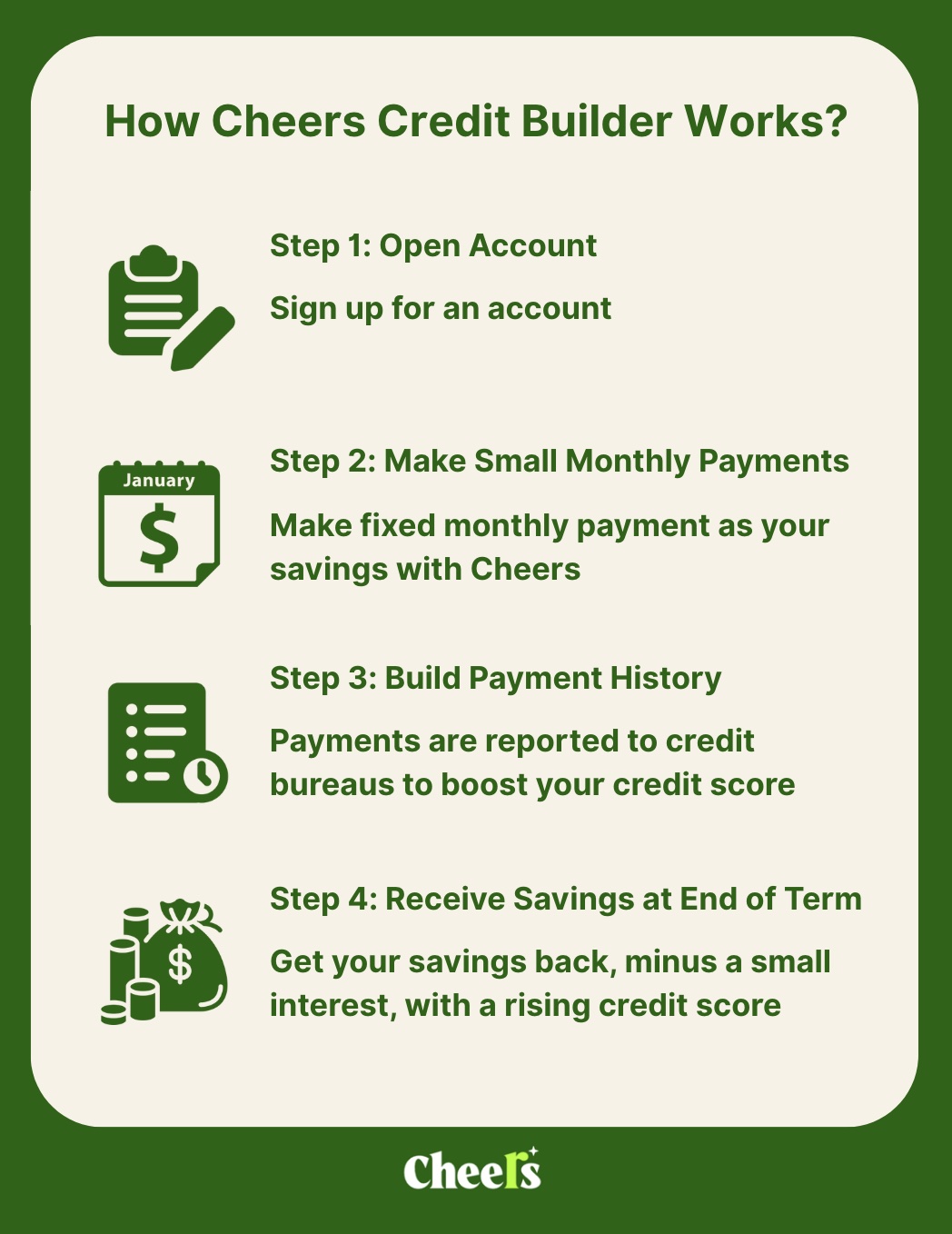

Secured cards and credit builder loans both aim to help people build credit, but they work differently. With a secured card, you’re borrowing against a deposit. With a credit builder loan, like the one offered by Cheers, you make fixed monthly payments into a locked savings account. The money is held until the end of your term, and your payments are reported to all three credit bureaus.

Unlike some secured cards, Cheers doesn’t charge annual or setup fees. There’s no credit check, just an ID match. You can start building credit with plans as low as $528, and at the end of the loan term, you get your savings back minus a small interest. The first payment is processed the following business day, which helps speed up the reporting process.

Getting Started with Cheers

If you’re new to credit or want to avoid the limitations of secured cards, Cheers might be a better fit. It’s designed to help people build credit while saving. There are no hidden fees, and the process is fast—sign-up takes just a few minutes.

Cheers reports your payments to all three major bureaus and helps you establish a positive payment history without needing a credit card. It’s a low-risk way to start building financial strength, especially if you’re concerned about credit card fees or limits.

Cheers is available in all 50 states and welcomes everyone, including immigrants and those who’ve never used credit before. It’s not a bank, but deposit accounts are held with FDIC-insured partner banks.

References

- Experian – What Is a Secured Credit Card?

- Experian – Credit Reports and Scores

- Equifax – Personal Credit Services

- TransUnion – Credit Monitoring and Reporting

- NerdWallet – Secured vs. Unsecured Credit Cards: What’s the Difference?

- FDIC - BankFind Suite