Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 6/8/2025

Table of Contents

- What Is a Business Credit Card?

- How to Use a Business Credit Card Wisely

- Building Credit with a Business Credit Card

- Managing Expenses Without the Stress

- Tracking Spending and Using Rewards

- Smarter Credit Starts with Smarter Tools

What Is a Business Credit Card?

A business credit card is designed to help you handle everyday business expenses while keeping your personal finances separate. Whether you run a side hustle or a small company, learning how to use a business credit card can simplify cash flow and build your credit.

Unlike personal cards, business cards often come with higher limits, employee card options, and benefits tailored to entrepreneurs. These cards may offer rewards on purchases like advertising, shipping, or software—expenses that matter most to your business.

If you’re just starting out, Experian explains that you can often apply as a sole proprietor using your Social Security number.

How to Use a Business Credit Card Wisely

To get the most out of your card, start by creating a plan. Use the card strictly for business-related expenses. This makes tax time easier and keeps your finances organized. The IRS outlines what qualifies as a business expense—things like office supplies, marketing tools, and travel.

Create a simple system for who can use the card, what it can be used for, and how purchases are tracked. If you have employees, many business card providers allow you to set spending limits on their cards.

Always pay your balance on time. If possible, pay it in full each month. This helps you avoid interest and builds a stronger credit profile.

Building Credit with a Business Credit Card

Understanding how to use a business credit card to build credit can benefit your business in the long term. Most business cards report activity to commercial credit bureaus, like Dun & Bradstreet or Experian Business. Some also report to personal bureaus, so good habits help both profiles.

Your credit utilization ratio—how much of your credit you’re using—matters. Try to keep it below 30% of your total limit. This tells lenders you’re using credit responsibly without relying on it too heavily.

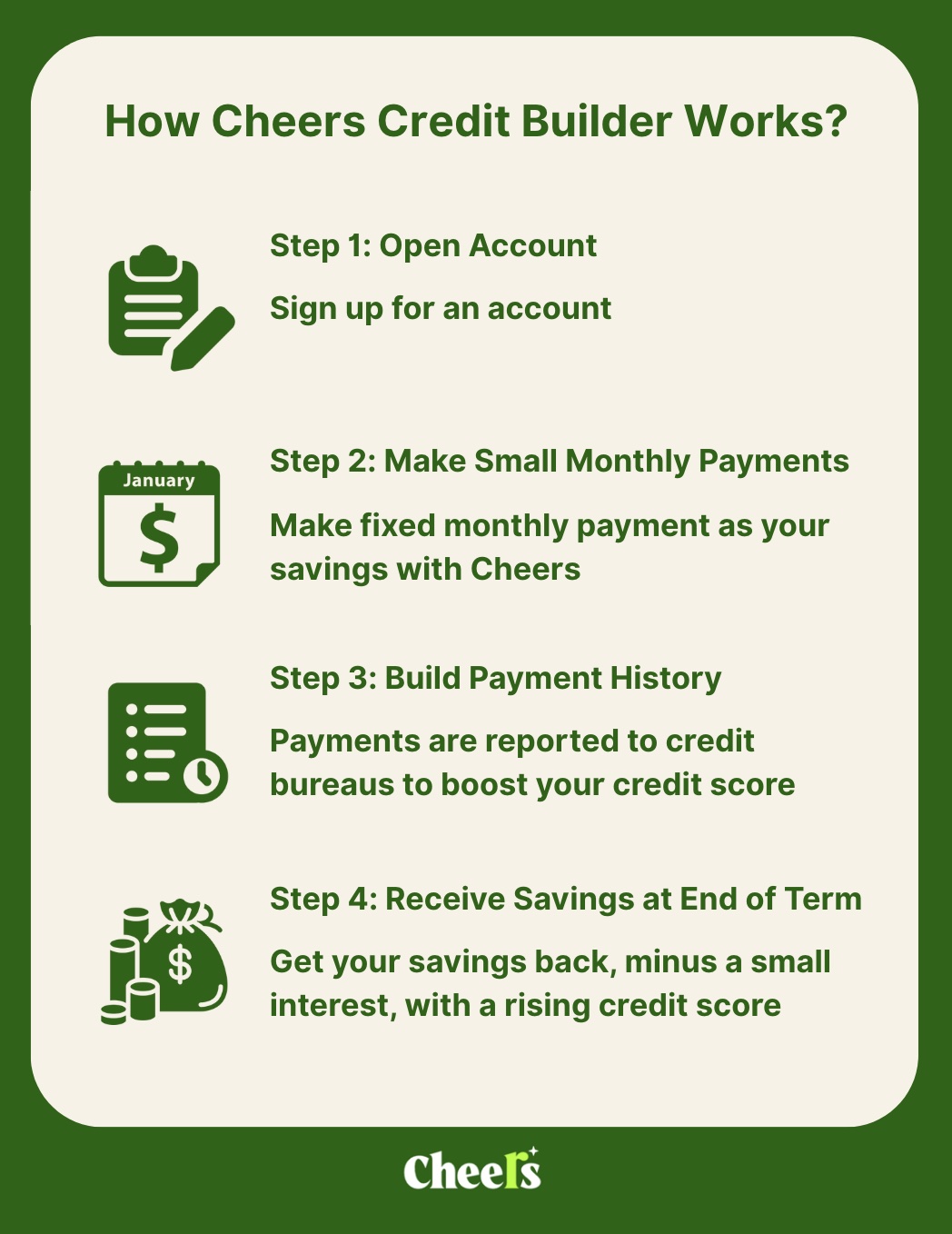

If you're new to credit or want to grow your score faster, consider pairing your business card with a tool that builds installment credit, like a credit builder loan. The Consumer Financial Protection Bureau (CFPB) explains how these loans help you establish a track record of on-time payments.

Managing Expenses Without the Stress

Using a business credit card can simplify your bookkeeping. Many cards offer categorized spending reports and integrations with accounting tools, such as QuickBooks or Xero.

Set up automatic payments for recurring bills, and review your monthly statements to catch errors or fraud early. You can also activate alerts to track spending in real-time. If a charge looks off, report it immediately—most card issuers offer protection for unauthorized transactions.

If you travel for work, consider finding a card that includes travel insurance or has no foreign transaction fees. Choose rewards that align with your actual spending, not ones that tempt you to overspend.

Tracking Spending and Using Rewards

Another benefit of knowing how to use a business credit card is maximizing rewards. Whether it’s cash back, travel points, or discounts on tools your business already uses, these perks can add up. Just be careful not to chase rewards at the cost of overspending.

Also, look for cards with built-in security tools—like virtual cards, fraud alerts, and spending limits by category. According to the Federal Trade Commission, these features reduce risk and protect your finances.

Most issuers provide a year-end spending summary, making budgeting and tax preparation much easier.

Smarter Credit Starts with Smarter Tools

Figuring out how to use a business credit card isn’t just about swiping smarter—it’s about setting up your business for long-term success. Used correctly, a business card helps you stay organized, earn rewards, and improve your credit score.

For those who are just starting to build credit—or want a boost without relying only on credit cards—products like credit builder loans can be a smart addition. They allow you to build payment history and save at the same time.

That’s where Cheers comes in. Cheers is a credit builder loan that reports to all three major credit bureaus and doesn’t require a credit check to get started. There are no setup or membership fees—just a simple low interests. It’s built to help people build credit on autopilot while saving in a secure, FDIC-insured account. Whether you're launching a new business or simply want to take control of your credit, Cheers provides a straightforward way to get started.

Alt Text: Infographic on How Cheers Credit Builder Works | www.cheers.credit

References