There's more than one way to save money-and the account you choose can shape how fast you grow it, how easily you access it, and whether it works with your other financial goals. From traditional savings accounts at local banks to high-yield options offered by online platforms, each type serves a distinct purpose. Some accounts are built for flexibility, while others are designed for higher returns. Some are good for organizing goals or saving money, while others, like Cheers Credit Builder, even help build your credit while you save. This guide breaks down the most common types of savings accounts, explains what they're best suited for, and enables you to determine which one fits your needs today. You don't need to be a financial expert to make a smart choice-you need to know where you are and where you're trying to go.

Why the Type of Saving Account You Choose Matters

Not all savings accounts are built the same. Some are great for emergencies. Others are better for earning a higher return over time. Some serve specific purposes, such as helping you stick to goals or automate habits.

However, what's often overlooked in the savings conversation is how choosing the correct account can either help or slow down your overall progress. For example, locking money away in a certificate of deposit (CD) might earn you more interest, but it limits access if you need to cover an unexpected bill.

And if you're trying to start saving consistently for the first time, too many options can be overwhelming.

So how do you decide?

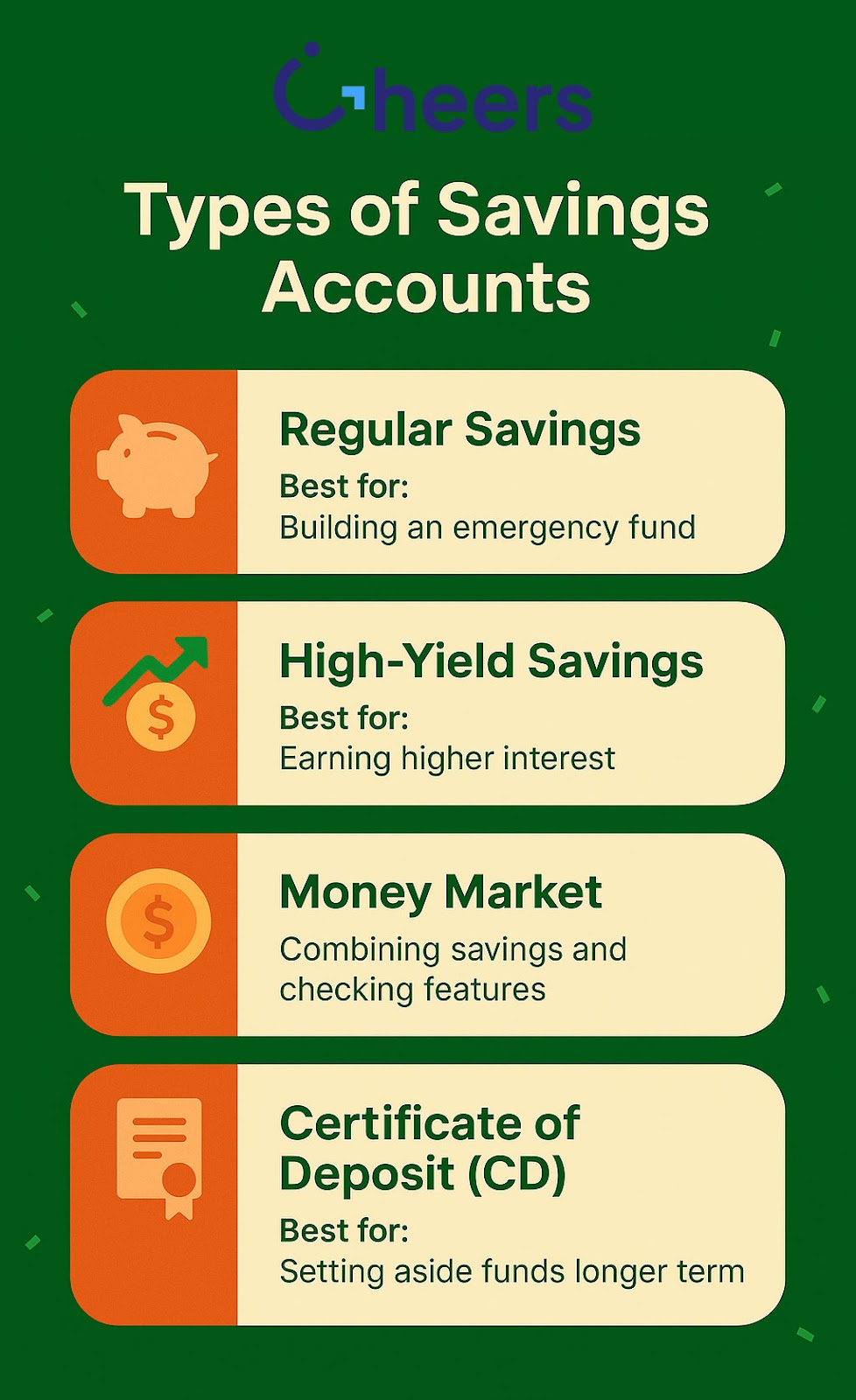

1. Traditional Savings Account

Best for: Beginners, basic savings, or linking with a checking account.

Traditional savings accounts are the most common type offered by banks, credit unions, and neobanks. They're FDIC-insured, usually have low or no minimum balances, and let you transfer money easily between checking and savings.

The downside? These accounts typically offer very low interest rates (sometimes as low as 0.05%), so your money does not grow significantly.

Pros:

- Simple and accessible

- Easy to open

- Suitable for short-term savings goals

Cons:

- Low interest

- Some may require minimum balances to avoid fees

2. High-Yield Savings Account

Best for: Keeping funds accessible while earning a considerable interest rate. Online banking typically offers high-yield savings accounts that pay a considerably higher interest rate than standard savings accounts. This can be an excellent option for building an emergency fund or growing savings without direct investment.

Pros:

- Higher interest returns

- Usually, there are no monthly fees

- Fast digital access

Cons:

- Sometimes, there is no branch access

- Some limits on transactions per month

3. Money Market Account

Best for: People who want to earn interest and occasionally write checks.

Money market accounts blend features of checking and savings. Typically, with higher interest rates, you may also have to move money out of the account. This account is generally suitable for consumers with higher balances who need to move money around more frequently than a high-yield savings account; however, they may require a minimum deposit.

Pros:

- Better interest rates than traditional accounts

- Check-writing or debit card access

- Safe and insured

Cons:

- Higher balance requirements

- May include monthly maintenance fees

4. Certificates of Deposit (CDs)

Best for: Longer-term savings goals that don't require frequent transfers of money from their account. CDs typically have a fixed interest rate over a specified time frame, ranging from around 6 months to 5 years. Agreeing to keep the money in the account, you typically earn a higher return on your savings account. Conversely, if you withdraw your funds early, you usually incur additional fees.

Pros:

- Locked-in, higher interest rate

- Encourages saving discipline

- Safe, low-risk

Cons:

- No flexibility

- Penalties for early withdrawal

They're not ideal for beginners or anyone who may need quick access to funds.

5. Goal-Based or Bucket Savings Accounts

Best for: People who want to organize and visualize their savings goals.

Some online banks and apps let you set up "buckets" or "goals" within a single savings account. You can name each one (like "vacation" or "emergency fund") and assign how much you want to save in each.

This isn't a different type of account, technically-it's a new way of using one.

Pros:

- Easier to plan and stick to goals

- Helpful for budgeting

- Encourages saving in multiple areas at once

Cons:

- Usually only available through specific platforms

- May not offer the highest rates

6. Credit-Building Savings Tools (Like Cheers Credit Builder)

Best for: People building or rebuilding credit while saving money.

This isn't a traditional savings account, but it's worth noting.

Cheers Credit Builder is a credit-building loan that helps you build your credit history while saving. You make monthly payments toward a locked savings account. Your payments are reported to all three credit bureaus to help build your score, and at the end of the term, you get your money back (minus interest).

Unlike savings accounts that don't affect your credit score, Cheers can support both your savings habit and your credit profile.

Pros:

- No credit check to start

- Builds payment history

- Funds returned at the end of the loan

- FDIC-insured savings

Cons:

- Can't access funds until the end of the term

- Interest charged monthly (though it's just 1% APR)

- Cheers is not a bank. Deposit accounts held by Sunrise Bank, Member FDIC.

Matching the Account Type to Your Goal

Choosing the correct savings account depends on what you need most right now. For starters, a traditional or high-yield savings account is the most standard option to build good savings habits. If your goals are short-term or involve emergencies, high-yield and goal-based savings buckets can help you achieve those specific objectives. On the other hand, for savings with a higher return, a CD may be a better option. If you want to build your credit, credit builder loans like Cheers are a great way to establish your credit profile while saving. Lastly, if you want to earn a considerable interest while moving money around, money market accounts may be the best option.

Start Where You Are, Not Where You Think You Should Be

Don't overthink the decision to get started. The best savings account for you is the one that encourages you to save consistently. As your finances grow, so will your options. And if you're ready to build credit alongside your savings, Cheers provides a structured, low-cost way to move forward with both.

Ready to build credit while saving? Start building your credit with Cheers today.