By: Joyce Jiang (marketing and finance enthusiast, creative solutions, data storyteller)

Date: 5/31/2025

Table of Contents

- Introduction: Why This Question Matters More Than Ever

- The New Normal: Rising Expectations for Savings

- Real Story: From $0 to Financial Confidence

- Emergency Funds: Where to Start and How Much to Save

- Retirement Savings: What You Should Have by Each Age

- Top Saving Trends in 2025

- How to Build Credit at the Same Time?

- How Much Should I Have in Savings? Key Takeaways

How much should I have in savings? It's a question more people are asking as prices stay high, incomes feel stretched, and emergencies never wait. In 2025, the financial landscape is different-saving isn't just smart, it's necessary. Whether you're building a rainy-day fund or planning for retirement, knowing what's realistic can bring peace of mind.

Why Expectations Are Rising

For years, the benchmark was saving three to six months' worth of expenses. But with inflation, high rent, and expensive healthcare, many experts now recommend closer to six to nine months of emergency savings. That's not a luxury-it's survival.

According to the U.S. Bureau of Economic Analysis (bea.gov), the personal savings rate has climbed to 4.9% in 2025, the highest since the pandemic. But this doesn't tell the whole story. A Bankrate study showed that 73% of Americans still feel unprepared because their income barely covers basic needs.

So, how much should I have in savings to feel secure? For someone earning $60,000 a year, that could mean having $30,000 or more set aside. It sounds steep-but there's a way to get there.

Personal Story: From $0 to Stability

When Amy, a 26-year-old graphic designer in Austin, lost her job during a company-wide layoff, she had just $137 in savings and two weeks' worth of rent left. "I thought I had time to figure it out," she said, "but life didn't wait." She turned to side gigs and automated her savings-even rounding up debit card purchases to stash the change.

Two years later, she now has $7,000 in emergency savings. "That first $1,000 made me breathe easier," she shared. "Now I can handle a flat tire or a doctor visit without spiraling."

Her turning point? Using MyMoney.gov's budgeting tool and downloading a micro-saving app that didn't charge hidden fees. "I didn't need a million bucks-I just needed a plan."

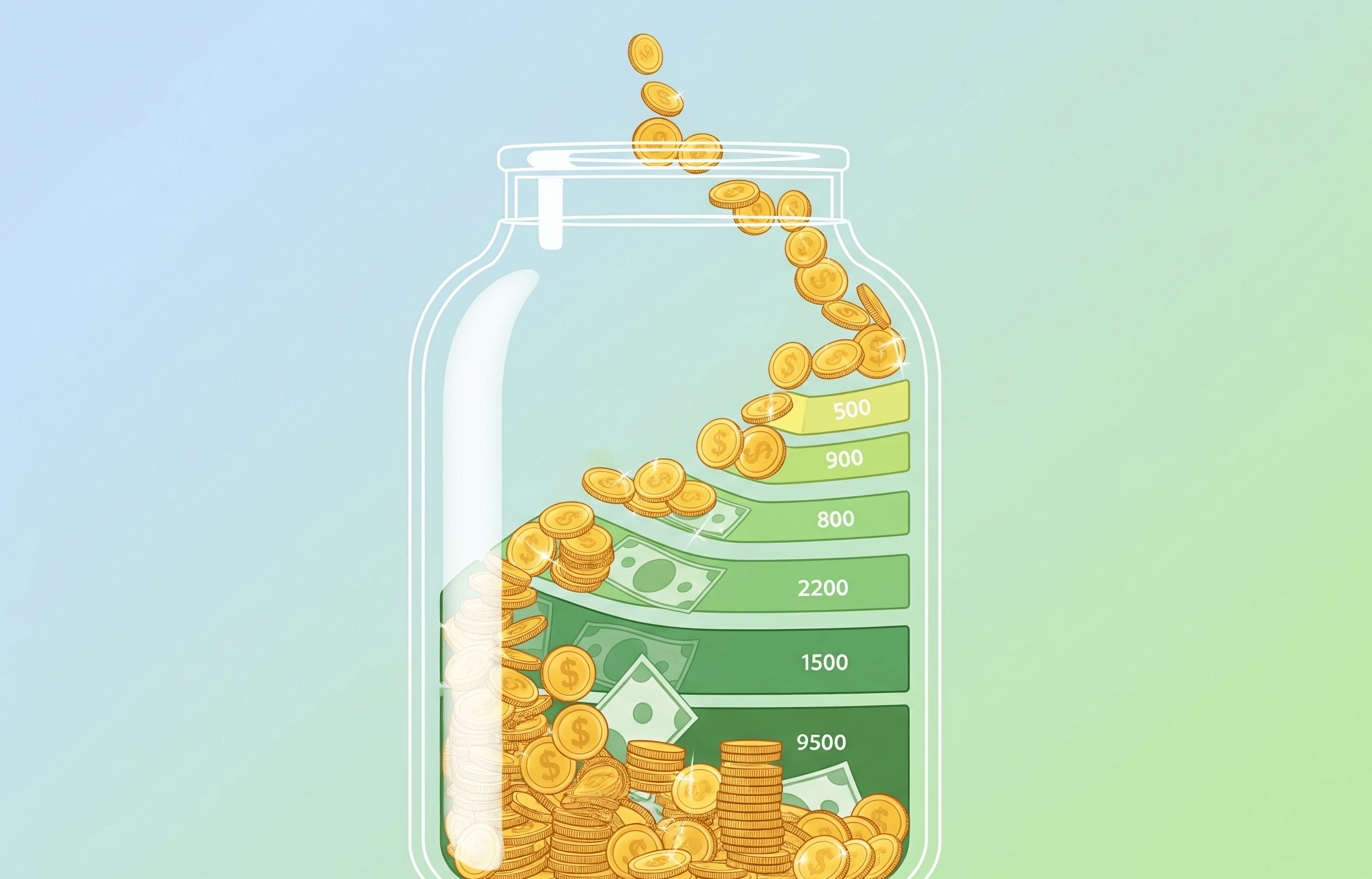

Emergency Funds: Where to Start

If you've ever asked "how much should I have in savings if something unexpected happens?", here's a simple breakdown:

- Starter goal: $500-$1,000

- Step two: 3 months of core expenses (rent, food, bills)

- Full fund: 6-9 months of total expenses

Use the free worksheet from the Consumer Financial Protection Bureau (consumerfinance.gov) to figure out your exact target.

Retirement: Changing Goals, Same Urgency

The amount people expect to need for retirement has actually dropped-down to $1.26 million in 2025 from $1.46 million a year ago, according to the Employee Benefit Research Institute (ebri.org). But lower expectations don't mean people are saving enough.

Many Gen X workers say they're supporting both their kids and parents while trying to build retirement savings. A 2025 survey showed that nearly half aren't confident they'll be able to retire when they hoped.

A good guide, according to the U.S. Department of Labor (dol.gov), is to aim for:

- By age 30: 1x your annual salary

- By 40: 3x

- By 50: 6x

- At retirement: 10-15x

2025 Trends: Saving Smarter, Not Harder

- High-yield savings accounts - With rates above 4.0%, they're giving savers a better return on liquid cash.

- Roth 401(k)s and IRAs - With future taxes expected to rise, more workers are paying taxes now for tax-free income later.

- Government-backed tools - MyMoney.gov and choosetosave.org offer free calculators to help you set retirement or emergency goals without upsells.

- Micro-saving apps - These roundup purchases and tuck away the difference. Paired with a structured plan, they help people like Amy get started even when budgets are tight.

How to Build Credit at the Same Time?

If you're building credit and savings at the same time, the Cheers Credit Builder account helps by reporting monthly to all three credit bureaus. There's no setup or membership fee-just a simple 1% monthly APR. You pick a repayment plan that suits your goals, and your payments are returned to you at the end of the term (minus the interest). Funds are FDIC-insured through Cheers's partner banks.

It's a good option for those without credit cards or for immigrants looking to build credit history. Signing up takes just a few minutes and doesn't require a hard credit pull.

* Cheers is not a bank. Deposit accounts held by Sunrise Bank, Member FDIC.

Read more about: How Do You Build Credit? A Simple Guide to Start Today

How Much Should I Have in Savings? A Recap

- Start with $500-$1,000

- Aim for 3-6 months of expenses

- Check your progress at life milestones (30, 40, 50+)

- Use tools that help automate and grow your savings

- Don't compare your journey to others-just start

How much should I have in savings? Enough to make you feel prepared, not panicked. Whether it's $1,000 or $100,000, what matters most is that you begin.