Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 6/8/2025

Table of Contents

- What Is a Subsidized Student Loan?

- What Is an Unsubsidized Student Loan?

- Main Differences

- Eligibility and FAFSA Impact

- Interest, Timing, and Cost

- Choosing a Loan That Fits

- Building Credit While Repaying Loans

If you're trying to figure out how to pay for college, federal student loans might be your first stop. The two main types you’ll encounter are subsidized and unsubsidized student loans. While both offer financial help, understanding their differences can help you avoid unnecessary debt and plan your repayment smarter.

What Is a Subsidized Student Loan?

A subsidized student loan is a federal loan available to undergraduate students with financial need. Its main feature is that the government pays the interest while you're enrolled at least half-time, during the grace period after graduation, and during approved deferment periods. This means you won’t owe more than what you borrow while in school, which helps reduce the total cost of your loan.

According to Federal Student Aid, these loans are need-based and offer lower overall costs for borrowers who qualify.

What Is an Unsubsidized Student Loan?

Unsubsidized student loans are available to both undergraduate and graduate students, and they don’t require proof of financial need. Interest starts accruing as soon as the loan is disbursed—even while you’re still in school. If you choose not to pay the interest while studying, it will be added to your loan balance once repayment begins, a process called capitalization.

You can read more about the structure of these loans on NerdWallet, which also includes repayment advice.

Main Differences Between Subsidized and Unsubsidized Student Loans

The key difference between subsidized and unsubsidized student loans is how interest works. With subsidized loans, the government covers your interest during school. With unsubsidized loans, you're responsible for interest from day one.

Subsidized loans are only available to undergraduates with demonstrated financial need, while unsubsidized loans are accessible to a broader range of students, regardless of their income. Both loans are part of the federal student loan program and have fixed interest rates, but the cost over time can vary a lot based on when interest starts.

Eligibility and FAFSA Impact

To get a subsidized student loan, you must fill out the Free Application for Federal Student Aid (FAFSA) and demonstrate financial need. Your school uses your Expected Family Contribution (EFC) and the cost of attendance to determine your eligibility for loans.

Unsubsidized loans also require FAFSA submission, but financial need isn't part of the equation. According to Bankrate, this makes unsubsidized loans more accessible, but potentially more expensive over time.

Interest Timing and Cost

This is where many students underestimate the long-term cost. For a subsidized student loan, no interest accrues while you're in school or during deferment. That helps keep your balance low. On the other hand, unsubsidized student loans rack up interest from the start. If you don’t make payments, you could owe far more than you borrowed.

Even though federal loan interest rates are relatively low, compounding interest can add thousands of dollars over time. Choosing subsidized loans whenever possible can help you save money and reduce your repayment burden.

Choosing a Loan That Fits

When offered both types of loans, it’s best to accept subsidized student loans first. They cost less over time and reduce your debt load after graduation. If your subsidized loan offer doesn’t cover all your expenses, you can then turn to unsubsidized loans before considering private loans.

Private loans often have higher rates, variable terms, and fewer protections. For most borrowers, federal loans offer better safety nets, such as income-driven repayment and forgiveness options.

Building Credit While Repaying Loans

Whether you have a subsidized or unsubsidized student loan, your repayment history is reported to credit bureaus. This means student loans can help you build your credit—if you make your payments on time.

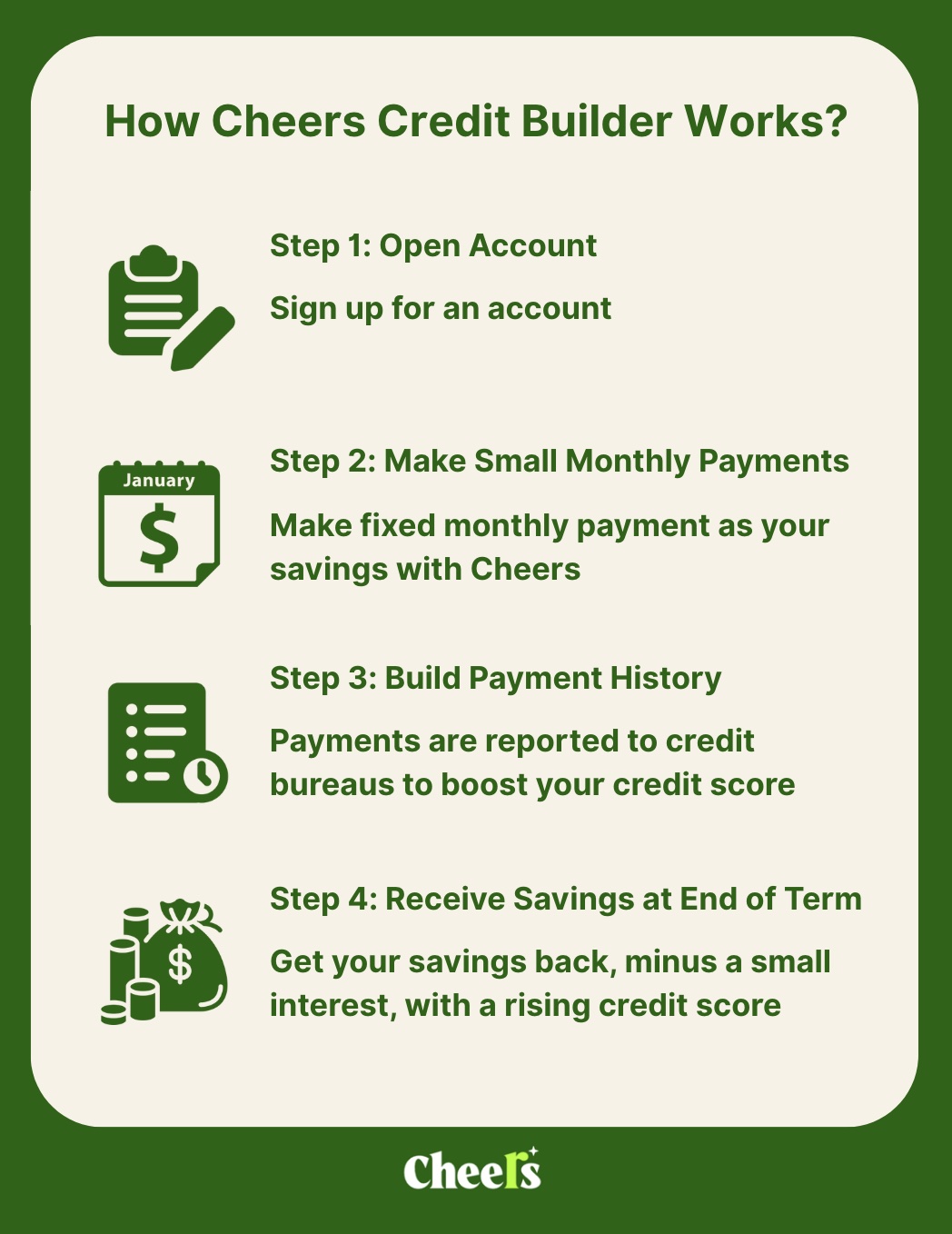

If you’re looking for more ways to strengthen your credit during or after school, consider options like the Cheers Credit Builder. It works by reporting your monthly payment activity¹ to all three major credit bureaus. There's no hard credit check, and you get your money back at the end of the term—minus interest. It's a simple and accessible way to build payment history alongside your student loan.

Final Thoughts

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

Understanding the difference between subsidized and unsubsidized student loans can protect you from unnecessary debt. Subsidized loans are better if you qualify, but both options offer support for your education goals. Before borrowing, always compare your options, focus on the timing of interest, and consider how repayment fits into your long-term credit and financial plan.

(The opinions expressed in this article are the author’s own and do not reflect the view of Sunrise Banks².)

References:

- Federal Student Aid – https://studentaid.gov/understand-aid/types/loans/subsidized-unsubsidized

- NerdWallet – https://www.nerdwallet.com/article/loans/student-loans/unsubsidized-student-loans

- Free Application for Federal Student Aid – https://studentaid.gov/h/apply-for-aid/fafsa

- Expected Family Contribution – https://studentaid.gov/help-center/answers/article/what-is-efc

- Bankrate – https://www.bankrate.com/loans/student-loans/subsidized-vs-unsubsidized-student-loans/

1 Payment activity:

All payment activity is reported to the credit bureaus. On-time payments may help build your credit, while late or missed payments may negatively impact it. Results are not guaranteed and depend on your individual financial behavior and credit profile.

² Sunrise Banks:

Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval. Must be at least 18 years old, have a valid U.S. bank account, and a Social Security Number.