Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 6/8/2025

Table of Contents

- Grocery Costs Are Getting Harder to Manage

- Smart Grocery Spending by Income

- What Current Trends Say About Shopping Habits

- Tips to Lower Grocery Costs Without Stress

- Why Food Budgets Matter for Credit Health

If you’ve ever asked yourself, how much should I be spending on groceries, you’re not alone. It’s one of the most common questions for anyone trying to stay on top of a budget. With prices rising and paychecks stretched thinner, grocery spending feels like it's getting harder to manage—even if you’re shopping the same as last year.

According to the USDA’s Food Plans, the monthly cost of groceries for a single adult on a Thrifty Plan ranges from approximately $297 to $372. A moderate plan can reach over $400. For a family of four, those monthly numbers jump to $996 or more (Ramsey Solutions). These benchmarks are helpful, but they’re not a one-size-fits-all solution.

Grocery Costs Are Getting Harder to Manage

Food inflation has made grocery bills unpredictable. Data from the Bureau of Labor Statistics show that the Consumer Price Index (CPI) for groceries (food-at-home) increased by 2.7% over the 12 months ending in August 2025, with categories such as meats, poultry, fish, and eggs rising the fastest (USDA (.gov)).

That’s only part of the story. Consumer preferences have shifted toward organic foods, convenience items, and specialized diets. These choices often come with higher price tags, making it even more challenging to estimate a fair grocery budget.

Smart Grocery Spending by Income

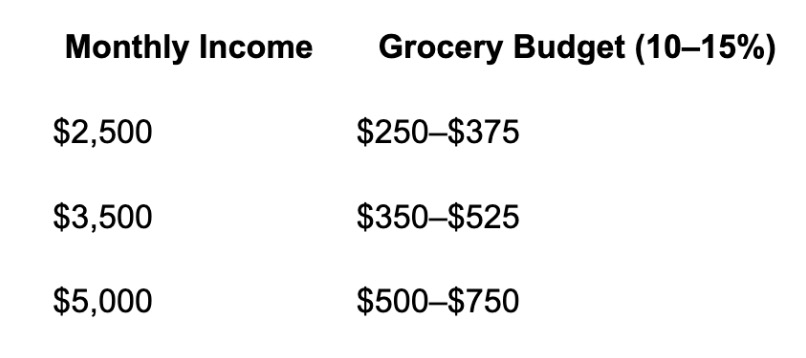

A helpful budgeting rule suggests spending about 10–20% of your after-tax income on groceries (Credit Counselling Society). For example:

These numbers are general, but they offer a solid foundation. Spending more than 15% may start to cut into your savings or debt payments. If you’re living in a high-cost city like Los Angeles or New York, your numbers might skew higher simply due to limited access to affordable food retailers.

Other factors also play a role—your cooking habits, how often you eat out, and whether you’re shopping for one or five people. It’s worth tracking your spending over a month to see where your personal average lands.

What Current Trends Say About Shopping Habits

More people are turning to meal-prepping and discount retailers to manage costs. Research from Morning Consult found a growing trend of consumers using meal planning as a strategy to save money. Coupon apps like Ibotta and loyalty programs at stores like Kroger or Safeway are also experiencing a surge in usage.

Another shift? Buying less but more often. Instead of a large weekly trip, some shoppers are breaking it into smaller visits to stay within budget. This also reduces food waste, which costs the average household more than $1,500 a year, according to ReFED.

Tips to Lower Grocery Costs Without Stress

If you’re trying to spend less without compromising on quality, start with a grocery list based on a weekly meal plan. Prioritize whole foods that can be used across multiple meals. For example, rice, beans, and frozen vegetables go far and store well.

Stick to store-brand items when you can—they often offer the same nutritional value as name brands. Shopping at local ethnic markets or discount grocers, such as ALDI, can also help shave dollars off your total.

Avoid shopping hungry or distracted, and check for digital deals before heading out. Programs like Double Up Food Bucks even match SNAP dollars at farmers' markets, further stretching low-income grocery budgets.

Why Food Budgets Matter for Credit Health

This content is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor or tax professional before making any financial decisions.

The money you spend on groceries can affect more than just your fridge. Overspending in this category often means pulling from savings, making late payments, or relying on credit cards. That can lead to missed payments, which directly impact your credit.

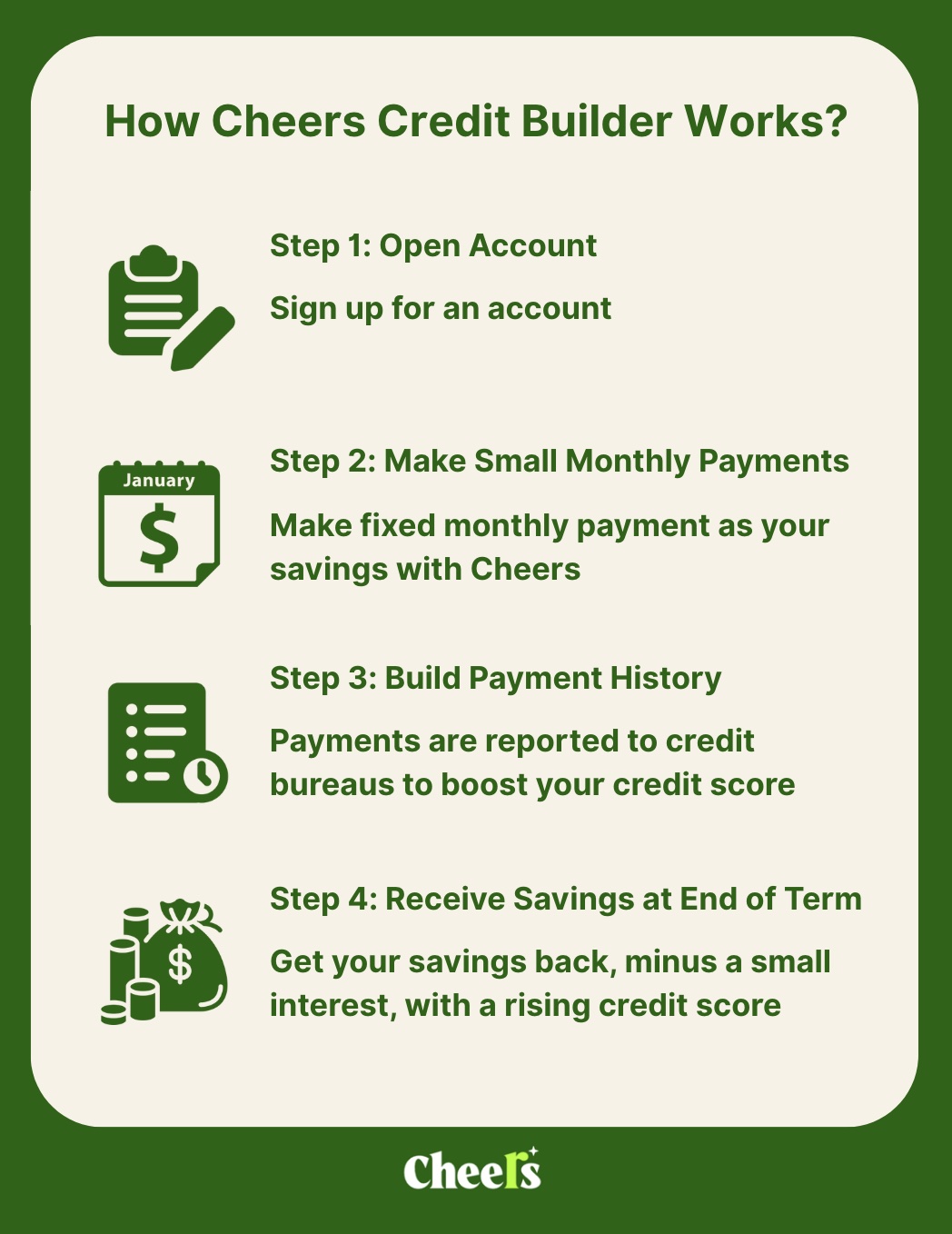

Budgeting wisely allows more room to focus on long-term goals—like building credit. If you’re just starting out or rebuilding, Cheers Credit Builder is a simple way to stay on track. With no hidden fees¹ and accelerated reporting, Cheers allows users to build more payment history (35% of your FICO® score²) by saving small amounts monthly. Your payments are securely held in a Certificate of Deposit (CD), with reporting your monthly payment activity³ to all three major credit bureaus.

How much I should be spending on groceries is more than just a budgeting question. It’s about knowing your limits, making smarter choices, and setting yourself up for bigger wins—whether that’s financial stability or a stronger credit score.

(The opinions expressed in this article are the author’s own and do not reflect the view of Sunrise Banks4.)

References:

- Ramsey Solutions – https://www.ramseysolutions.com/budgeting/average-cost-of-groceries#:~:text=The%20average%20grocery%20cost%20per,for%20a%20family%20of%20four.

- Bureau of Labor Statistics – https://www.bls.gov/news.release/cpi.nr0.htm#:~:text=Food%20The%20index%20for%20food,at%20home%20rose%201.5%20percent.

- USDA (.gov) – https://www.ers.usda.gov/data-products/food-price-outlook/summary-findings#:~:text=Between%20the%201970s%20and%20early,affected%20egg%20and%20poultry%20prices.

- Credit Counselling Society – https://nomoredebts.org/budgeting/budgeting-guidelines#:~:text=Consulting%20a%20financial%20advisor%20about%20your%20particular,taxis%2C%20fuel%2C%20vehicle%20insurance%2C%20maintenance%2C%20and%20parking

- Morning Consult – https://pro.morningconsult.com/analysis/grocery-spending-inflation-coupon-savings

- Ibotta – https://home.ibotta.com/

- Kroger – https://www.kroger.com/

- Safeway – https://www.safeway.com/

- ReFED – https://refed.org/uploads/consumer-food-waste-report-2025-final.pdf

- Double Up Food Bucks – https://doubleupamerica.org/

1 No Hidden Fees:

There are no application fees, maintenance fees, or early cancellation penalties.

² FICO® Credit Factors:

According to FICO®, 35% of your credit score is based on payment history, and 10% is based on credit mix. Cheers reports every payment and adds a secured installment loan to your profile. Source: myFICO: https://www.myfico.com/credit-education/whats-in-your-credit-score

³ Payment activity:

All payment activity is reported to the credit bureaus. On-time payments may help build your credit, while late or missed payments may negatively impact it. Results are not guaranteed and depend on your individual financial behavior and credit profile.

⁴ Sunrise Banks:

Cheers is a financial technology company and not a bank. Banking services are provided by Sunrise Banks N.A. Your funds are FDIC insured up to $250,000 through Sunrise Banks, N.A., Member FDIC. Results are not guaranteed. Improvement in your credit score is dependent on your specific situation and financial behavior. Failure to make monthly minimum payments by the payment due date each month may result in delinquent payment reporting to credit bureaus, which may negatively impact your credit score. This product will not remove negative credit history from your credit report. All loans are subject to approval. Must be at least 18 years old, have a valid U.S. bank account, and a Social Security Number.