Author: Vince Adriatico (Ex-banker with 750+ Credit Score)

Date: 5/6/2025

Table of Contents:

- The Roadblock: What Is Mortgage Insurance?

- The Big Question: How Much Is Mortgage Insurance?

- Conventional Loans (PMI)

- FHA Loans (MIP)

- The Plan: How Long You'll Pay It

- PMI (Conventional Loans)

- MIP (FHA Loans)

- How to Lower or Avoid It

- The Win: Turning Confusion Into Clarity

- Next Step: Build Credit Before You Buy

You've finally found a home that feels right. You're ready to leap, but then the numbers come in. And right in the middle of your mortgage estimate is a line you didn't plan for: mortgage insurance. What is it? Why do you need it? And most importantly, how much is mortgage insurance going to cost you? If you're putting down less than 20%, mortgage insurance is probably part of your loan. But don't let it throw off your homebuying momentum. This guide breaks down what it is, how it works, what it costs, and how to make it work for you, not against you.

The Roadblock: What Is Mortgage Insurance?

Mortgage insurance isn't there to protect you-it- it's for your lender. But it's often the key that unlocks homeownership when you don't have 20% down.

There are two main types:

- PMI (Private Mortgage Insurance) for conventional loans

- MIP (Mortgage Insurance Premium) for FHA loans

Both come with a monthly cost and sometimes an upfront fee. But they're also what makes lower down payments possible. Understanding the differences helps avoid surprises and gives you more control over your monthly payments.

The Big Question: How Much Is Mortgage Insurance?

You don't want vague answers. You want numbers.

Conventional Loans (PMI)

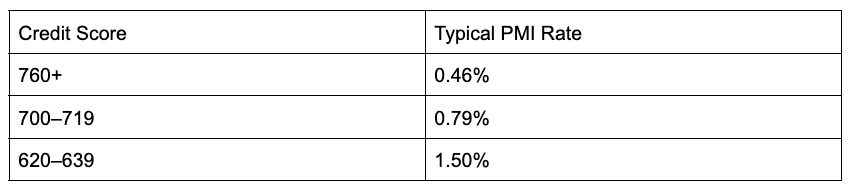

The cost of PMI depends heavily on your credit score and down payment. For most borrowers, you'll pay somewhere between:

- 0.46% and 1.50% annually of the loan

- That's $115 to $375/month on a $300,000 mortgage

The higher your credit score, the lower your rate. Here's a snapshot:

Run the numbers for yourself with NerdWallet's PMI calculator.

FHA Loans (MIP)

FHA loans take a different approach. You'll pay:

- Upfront MIP: 1.75% of the loan (can be rolled in)

- Annual MIP: 0.45% to 1.05%, paid monthly

On a $300,000 FHA loan, that's:

- $5,250 upfront

- $112 to $262/month

The CFPB's FHA insurance explainer breaks this down in simple terms.

The Plan: How Long You'll Pay It

PMI (Conventional Loans)

You're not stuck with PMI forever. It goes away once you've built up equity:

- Automatically removed when your LTV hits 78%

- You can request removal at 80% LTV if you're in good standing.

- Or refinance once your home value rises.

MIP (FHA Loans)

FHA is less flexible. If you put down less than 10%, you'll likely pay MIP for the life of the loan. With 10% or more, it can drop off after 11 years. Many FHA borrowers later refinance into conventional loans to remove it.

How to Lower or Avoid It

You're not powerless here. There are ways to avoid or reduce mortgage insurance:

- Save for 20% down; it eliminates PMI entirely

- Boost your credit score- lower scores usually mean higher insurance

- Look into lender-paid PMI, but check how it affects your rate

- Explore an 80/10/10 piggyback loan if your bank offers it.

These aren't just financial hacks-they're paths to reclaiming more control over your home loan.

The Win: Turning Confusion Into Clarity

When buying a home, surprises are the last thing you need. If you're wondering how much mortgage insurance is, the answer depends on your situation, but it doesn't have to be a mystery. You've got tools, options, and a game plan. And with the right credit strategy, you can lower the cost or avoid it altogether.

Next Step: Build Credit Before You Buy

If you're not quite there yet on your credit score or savings, there's still forward momentum you can create. Cheers Credit Builder helps you build credit month by month, with no hidden fees, no credit check, and no need for a credit card. It reports your payments to all three credit bureaus while you save in an FDIC-insured account.

Disclaimer: Loan terms, mortgage insurance rules, and costs vary by lender and borrower. Always review your loan estimate carefully and speak with a licensed mortgage advisor.