Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 5/11/2025

Table of Contents

- Understanding Your Credit Score

- Paying Bills On Time Isn’t Optional

- How Credit Cards and Loans Affect Your Score

- Rent, Buy Now Pay Later & Alternative Data

- Autopilot Credit Building with Cheers

- Final Thought: Stay Patient, Stay Consistent

Building credit is one of those things you don’t think about—until you need it. Whether it’s getting approved for an apartment, buying a car, or qualifying for a lower interest rate, your credit score can either open doors or close them. If you’ve ever asked yourself “how do I build my credit score?”, you’re not alone—and you’re not behind.

Let’s walk through how credit scores work and how you can start improving yours with tools designed for real life.

Understanding Your Credit Score

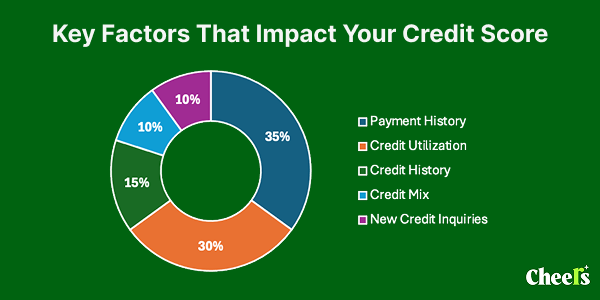

Before taking any action, it’s helpful to know what makes up your credit score. The most common credit score used by lenders is the FICO score, which ranges from 300 to 850. Here’s a rough breakdown:

- 35% Payment History: Whether you pay your bills on time.

- 30% Credit Utilization: How much of your available credit you're using.

- 15% Length of Credit History

- 10% Credit Mix: Types of credit (installment loans, credit cards).

- 10% New Credit Inquiries: How often you apply for credit.

So when you wonder, “how do I build my credit score?”, you’re really asking how to influence these five factors in a positive way.

Paying Bills On Time Isn’t Optional

Late payments can stay on your credit report for up to seven years. That’s why consistent on-time payments matter most. Start by setting up auto-pay on your bills. This includes student loans, phone bills, utilities, and any credit cards you use.

You can also use tools that help you automate this process. Several banking apps and services now send reminders or even automate payment scheduling based on your payday.

How Credit Cards and Loans Affect Your Score

Opening a secured credit card or credit builder loan is one of the first steps many people take to build their credit score. But using these tools wisely is key.

With credit cards:

- Don’t use more than 30% of your credit limit

- Always pay more than the minimum balance

- Keep accounts open as long as possible

If you’ve never had a loan before, a credit builder loan might be a smart choice. These work differently from traditional loans. You don’t get the money upfront. Instead, your payments are held in a secured account and reported to credit bureaus monthly. When the loan ends, you get the money back—minus interest.

This is where Cheers Credit Builder can help. It’s designed to help people build credit without needing a credit check, and reports monthly payments to all three major credit bureaus. Your repayment history starts being reported almost immediately—faster than many competitors—so you can begin building positive credit data from day one.

Rent, Buy Now Pay Later & Alternative Data

A big credit trend in 2024 and 2025 is using alternative data to build your credit score. This includes:

- Rent reporting: Services like Experian RentBureau allow landlords or tenants to report on-time rent payments.

- Buy Now Pay Later (BNPL): Companies like Affirm and Afterpay now report on-time payments to credit bureaus.

- Streaming and utility bills: Through programs like Experian Boost, you can add Netflix, phone bills, and more to your report.

These won’t impact your score as strongly as traditional credit lines, but every point counts—especially when you’re starting from scratch.

Autopilot Credit Building with Cheers

If you're looking for a hands-off way to build your credit score, Cheers Credit Builder stands out. It’s a small monthly installment loan—starting as low as $528—designed to help you establish payment history while saving money. There are no hidden fees, no hard credit checks, and the APR is a flat 12% annually. All funds are held in an FDIC-insured account until your term ends.

Cheers reports to all three bureaus and begins doing so after your first payment, which is processed the next business day. That speed makes a difference if you're trying to make progress quickly.

Cheers is not a bank. Deposit accounts are held by Sunrise Bank, Member FDIC.

It’s also ideal for those who don’t want to rely on credit cards or may not qualify for traditional credit lines yet. You’ll build credit while saving—not spending.

Learn more and sign up at Cheers.Credit

Final Thought: Stay Patient, Stay Consistent

As tempting as it is to want fast results, credit building doesn’t happen overnight. But if you’re asking “how do I build my credit score?” and you’re willing to take action, you’re already ahead. Focus on building habits—on-time payments, low credit usage, and smart use of tools like Cheers—and the score will follow.

Want help building your credit automatically? Sign up for our newsletter and start your credit journey with Cheers.

External Souce: